Our Terms & Conditions | Our Privacy Policy

The big switch: Institutional investors snap up stocks that retail investors are exiting

Institutional investors, such as foreign institutional investors (FIIs) and domestic institutional investors (DIIs), often have access to in-depth research and resources that most retail investors don’t. Their moves can hint at underlying strengths in a company that might not be immediately visible.

Let us take a look at the companies where FIIs and DIIs are increasing their stakes while retail investors are pulling back. What’s catching the eye of these big players, and should you be paying attention too?

1. Britannia Industries Ltd

Britannia Industries has strengthened its position as one of India’s top food companies through a century of operation. Known for its commitment to quality, the company offers a wide range of products, including biscuits, bread, cakes, rusk, and dairy items, making it a staple in Indian households.

Investment Activity (2021 to present):

⦁ FIIs: Stake largely constant.

⦁ DIIs: Increased holdings from 11.5% to 16.3%.

⦁ Retail investors: Reduced stake from 20.3% to 15.1%.

Britannia has achieved a compounded annual growth rate (CAGR) of about 13% over the last five years.

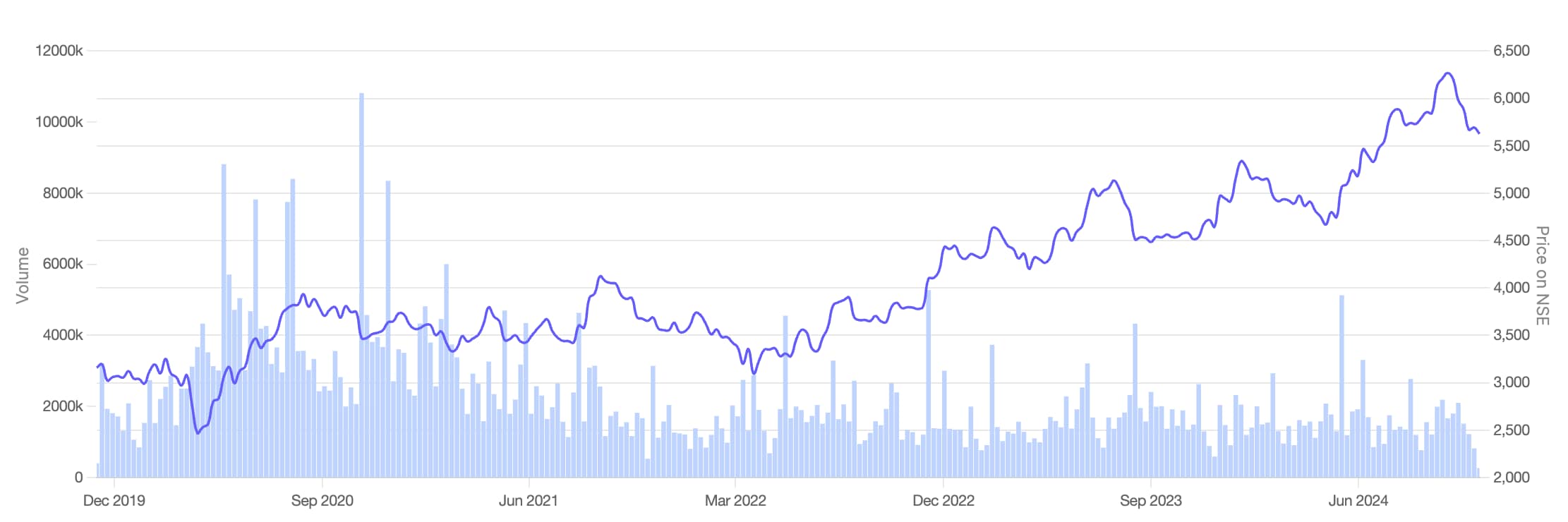

Britannia Industries Share Price Chart (Nov ‘19 till Oct ‘24)

View Full Image

Source: Screener.in

Why are institutional investors interested?

Institutional investors are particularly drawn to Britannia Industries because of its impressive performance over the past five years.

Britannia’s sales have soared from ₹11,055 crore in March 2019 to ₹16,769 crore by March 2024, marking a robust 52% absolute growth and a compounded annual growth rate (CAGR) of about 9%.

This growth has been fueled by their strategic focus on innovation, expanding into rural markets, and launching new products like health-oriented NutriChoice range.

The company’s Ebitda has also surged from ₹1,733 crore to ₹3,170 crore, reflecting a CAGR of 13%, and net profit grew from ₹1,159 crore to ₹2,140 crore at the same rate. The faster profit growth rate compared to sales underscores Britannia’s effective cost-control measures.

With a return on capital employed (RoCE) at an impressive 54%—well above the industry median of 22%—it’s clear why institutions find Britannia a highly efficient bet in using capital to generate profits. The company’s attractive dividend payout ratio of over 40% makes it a preferred pick for investors seeking regular income.

What’s up with retail investors?

Retail investors seem to be stepping back from Britannia Industries, likely influenced by the stock’s significant appreciation.

From about ₹2,750 in 2019 to ₹5,600 in October 2024, the price surge might have led many to cash in on their investments, particularly if they suspect the stock’s short-term growth potential might be capped.

Currently, Britannia trades at a price-to-earnings (PE) ratio of 60x, which towers over the industry average of 35x. This lofty valuation could lead some retail investors to perceive the stock as overpriced relative to its earnings scope, prompting them to reallocate their funds to other high-growth opportunities, though whether these shifts are proving beneficial remains to be seen.

2. ITC Ltd

ITC is a prominent Indian conglomerate with a diversified presence across industries such as fast moving consumer goods (FMCG), hotels, paperboards, packaging, agribusiness, and information technology. Known for brands like Aashirvaad, Sunfeast, Bingo!, and Classmate, ITC has become an integral part of daily life for millions of Indians.

Investment Activity (2021 to present):

⦁ FIIs: Increased holdings from 9.9% to 40.5%.

⦁ DIIs: Stakes largely constant.

⦁ Retail Investors: Reduced holdings from 46.2% to 14.8%.

ITC has achieved a CAGR of about 14% over the last five years, focusing on expanding its non-tobacco FMCG business.

ITC Ltd Share Price Chart (Nov ‘19 till Oct ‘24)

View Full Image

Source: Screener.in

Why are institutions interested?

One of the main attractions is the significant growth in ITC’s non-tobacco FMCG segment. Brands like Aashirvaad, Sunfeast, and Bingo have become market leaders in their categories, contributing over ₹15,000 crore in revenues. Institutions see this shift towards high-growth areas as a strategic move that positions ITC for substantial future gains.

Financial performance is another key factor.

ITC’s revenue grew from ₹48,353 crore in March 2019 to ₹70,881 crore in March 2024, marking an absolute growth of 47%. The steady increase in Ebitda from ₹18,425 crore to ₹26,232 crore reflects consistent profitability, which is a crucial consideration for institutional investors.

Moreover, ITC offers a generous dividend payout ratio of 80%, making it attractive for investors seeking regular income. Such a high payout is significantly above the industry median and appeals to institutions like pension funds and insurance companies.

Additionally, the company’s robust agri-business provides a strategic advantage, especially given the importance of agriculture in India’s economy. ITC’s deep involvement in this sector not only contributes to its revenues but also positions it favourably in terms of rural engagement and supply chain integration.

Institutions could also be factoring in the potential for unlocking shareholder value through corporate restructuring. There’s market speculation about ITC potentially demerging its businesses, which could lead to value creation. Institutional investors often position themselves ahead of such developments to capitalise on potential upside.

Lastly, the anticipated recovery of the hospitality sector post-pandemic adds another layer of growth potential for ITC. As travel and tourism pick up, the company’s hotel business is expected to contribute positively to its overall performance, offering additional benefits for investors.

What’s up with retail investors?

Historically, ITC’s stock price remained relatively flat for extended periods, which may have led retail investors to seek better-performing investments.

Retail investors might also prefer investments that offer quicker capital appreciation over those that provide high dividend payouts. Although ITC has a generous dividend payout ratio of 80%, some investors might prioritise growth over income, especially in a bullish market environment where other stocks are delivering substantial gains.

Also Read: The Magnificent 7: Why Indian investors are eyeing these US giants

3. Infosys Ltd

Infosys is a global leader in next-generation digital services and consulting. Established in 1981, the company has grown to become a key player in the IT services industry, offering solutions in areas such as cloud computing, artificial intelligence, data analytics, and cybersecurity.

Investment Activity (2021 to present):

⦁ DIIs: Increased holdings from 16.3% to 37.8%.

⦁ FIIs: Stake largely constant.

⦁ Retail Investors: Reduced holdings from 37.1% to 14.1%.

Infosys has achieved a CAGR of about 21% over the last five years.

Infosys Share Price Chart (Nov ‘19 till Oct ‘24)

View Full Image

Source: Screener.in

Why are institutions interested?

As a global leader in next-generation digital services and consulting, Infosys is at the forefront of technological innovation, helping clients in over 50 countries navigate their digital transformation journeys.

The company’s strong financial performance is a significant draw.

From March 2019 to March 2024, Infosys’s revenue surged from ₹82,675 crore to ₹1,53,670 crore, marking an absolute growth of 86%. Net profit increased from ₹15,404 crore to ₹26,233 crore, showcasing a CAGR of 11%. Such consistent and substantial growth is highly appealing to institutions seeking reliable returns.

Institutions also recognize that the company is strategically placed to benefit from the increasing investment by businesses worldwide in technology to improve efficiency and competitiveness.

The company also maintains healthy margins and returns, with a return on capital employed (RoCE) of over 35%, above the industry median of nearly 20%. This indicates efficient use of capital and strong operational performance, both of which are critical factors for institutional investors.

Additionally, Infosys has a strong balance sheet with substantial cash reserves and minimal debt. This financial stability allows the company to invest in growth opportunities, pursue strategic acquisitions, and return capital to shareholders, all of which are favourable from an institutional investment perspective.

What’s up with retail investors?

Retail shareholding in Infosys has decreased significantly, and this could be due to a combination of factors.

The stock price has more than doubled from ₹700 in 2019 to ₹1,800 level in October 2024. Such substantial appreciation provides an opportunity for investors to realise profits, which many may have chosen to do.

Additionally, Infosys is trading at a PE ratio of 25x, slightly above the industry average of 22x. Some retail investors might view the stock as fairly valued or even overvalued, leading them to believe that future growth might be limited or that the stock could be susceptible to a price correction.

Global economic uncertainties, such as changes in outsourcing trends or geopolitical tensions, might also make some investors cautious about holding large positions in established IT firms like Infosys.

For more such analysis, read Profit Pulse.

4. Crisil Ltd

Crisil is a leading analytics company providing ratings, research, and risk advisory services.

Investment Activity (2021 to Present):

⦁ DIIs: Increased holdings from 6.3% to 12.7%.

⦁ FIIs: Stake largely constant.

⦁ Retail Investors: Reduced holdings from 19.9% to 13.4%.

The company has achieved a CAGR of about 31% over the last five years.

Crisil Share Price Chart (Nov ‘19 till Oct ‘24)

View Full Image

Source: Screener.in

Why are institutions interested?

Institutions are attracted to Crisil’s stable and recurring revenue model. The demand for credit ratings and financial analytics is growing, especially as financial markets expand and regulatory requirements become more stringent. Crisil’s services are often mandated by regulations, providing steady stream of business and revenue stability.

The company’s financial performance is also a significant factor.

Crisil’s revenue grew from ₹1,732 crore in March 2019 to ₹3,142 crore in March 2024, marking an absolute growth of 82%. EBITDA increased from ₹456 crore to ₹882 crore, reflecting a CAGR of 14%. This growth is with the premise that net profit margin is healthy at 20%.

Crisil’s RoCE is 40%. This is actually solid considering how industry is shaping and the corporate bond market is expanding.

Moreover, the company’s dividend payout ratio of 60% is attractive for investors seeking regular income. Such a high payout reflects CRISIL’s ability to generate consistent cash flows and its commitment to returning value to shareholders, aligning with the investment strategies of many institutions.

Crisil’s association with S&P Global enhances its credibility and global reach. This strategic partnership provides opportunities for international business and collaboration, which can lead to further growth and is a significant consideration for institutions investing with a global perspective.

Additionally, the high entry barriers in the credit rating industry protect CRISIL’s market position. The need for established credibility and stringent regulatory requirements makes it difficult for new competitors to enter the market, reducing competitive risks for investors.

What’s up with retail investors?

As a credit rating agency, Crisil’s operates in a niche market that may not offer the same growth opportunities as other sectors. Retail investors seeking higher returns might be shifting their investments to industries with stronger growth prospects, such as technology.

Market volatility and economic uncertainties can also impact the financial services sector. Retail investors might be reducing their exposure to mitigate potential risks, preferring to invest in companies they perceive as more resilient during economic downturns.

Should you follow the big investors?

So, we’ve seen that FIIs and DIIs are increasing their stakes in these companies while retail investors are stepping back. Does this mean you should jump on the bandwagon?

Well, it’s not that straightforward. Institutional investors have deep pockets, access to extensive research, and can afford to take a long-term view—even ride out storms that might shake off retail investors.

It’s essential to do your own homework. Consider adding these companies to your watchlist. Dive into their financials, understand their business models, and see if they align with your investment goals.

Remember, following institutional moves blindly isn’t a guaranteed recipe for success. However, studying their choices can provide valuable insights and perhaps help you spot the next big opportunity.

Also read: 5 stocks India’s Warren Buffetts just added to their portfolios

Note: We have relied on data from the Tijori Finance and respective company’s annual report throughout this article. For forecasting, we have used our assumptions.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.The views expressed are my own and do not reflect or represent the views of my present or past employers.

Parth Parikh has over a decade of experience in finance and research, and he currently heads the growth and content vertical at Finsire. He has a keen interest in Indian and global stocks and holds an FRM Charter along with an MBA in Finance from Narsee Monjee Institute of Management Studies. Previously, he has held research positions at various companies.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.