Our Terms & Conditions | Our Privacy Policy

1 Magnificent S&P 500 Dividend Stock Down 30%: 4 Reasons to Buy Public Storage in 2025 and Hold Forever

Between 2020 and 2022, leading self-storage real estate investment trust (REIT) Public Storage (PSA -2.19%) saw its share price more than double thanks to a pandemic-aided boom. Since then, however, Public Storage’s stock has dropped roughly 30% from its highs.

To be fair to Public Storage, nothing business-specific went wrong operationally. In fact, its sales have grown by 12% in total over the last two years. Yet, the REIT couldn’t muster enough cash generation amid a weaker self-storage environment to match the impressive financial results it delivered to investors in 2021 and 2022, leaving the market dismayed.

This cyclicality in the public storage industry, combined with a slight market overreaction, leaves Public Storage trading at a price that makes it one of my favorite high-yield S&P 500 stocks today. Here are the four reasons I’ll be adding to my position in the magnificent REIT in 2025.

4 Reasons to buy Public Storage in 2025

Powered by its famous bright-orange facilities and logo, Public Storage has grown to become the largest self-storage provider in the United States. To visualize just how powerful Public Storage’s network of locations is, consider that half of the U.S. population lives within a “trade area” of one of its facilities.

However, while this leadership advantage and vast scale are impressive in their own right, these four additional items make the REIT a top-tier investment worth holding for decades.

1. Best-in-class REIT

Public Storage might just be one of the best REITs available on the market.

First, from a financial well-being perspective, Public Storage holds the highest Moody’s and S&P Global credit ratings of any U.S. REIT. While this may elicit a yawn out of the market when compared to today’s world of artificial intelligence and quantum computing, this rock-solid foundation is what powers the company’s growth charge.

Since 2019, Public Storage has added 36% more square feet of storage space to its portfolio through $11.7 billion of investments in its facilities, thanks to its ability to secure funding at attractive rates.

Second, Public Storage was a first-mover in the self-storage industry as it quickly implemented a digital operating model. More than 2 million customers use the company’s mobile app today. This transformation allows the company to offer digital access, a digital care team, live help, and kiosks (also with live help) at each location instead of dozens of employees.

This digital prowess keeps the company top-of-mind among younger, tech-savvy generations, giving it an advantage when acquiring new customers. For instance, Public Storage generates 75% of its new customers through its digital eRental program, whereas its REIT peers’ average is only 30%.

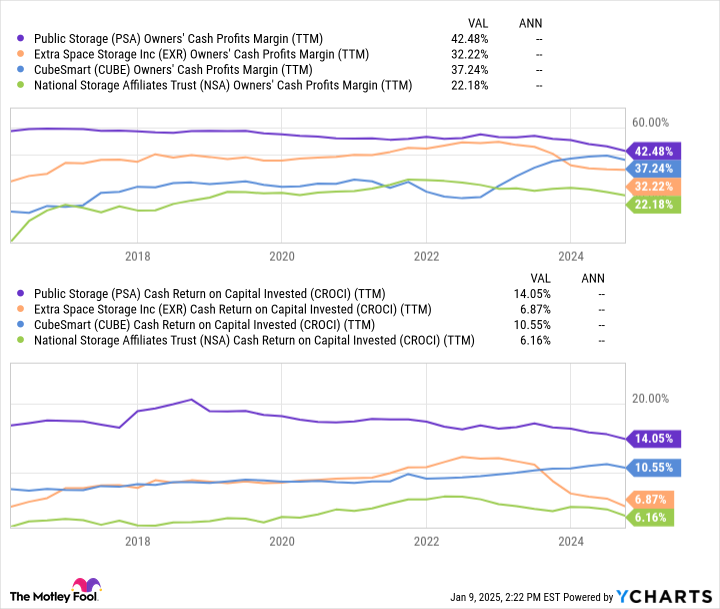

Finally, the company’s cash-generating capabilities remain superior compared to its self-storage peers.

PSA Owners’ Cash Profits Margin and Cash Return on Capital Invested (TTM) data by YCharts

Not only does Public Storage create more substantial free cash flows (FCF) from its current stores, but it also does a better job of generating cash from its debt and equity, as its higher cash return on invested capital (ROIC) suggests.

2. High return on invested capital in a fragmented market

Public Storage’s ability to generate outsized cash flows from new investments is crucial to investors interested in the company. Despite being the biggest self-storage provider in the United States, the company only holds a relatively minor 9% market share, leaving much room to continue accumulating its share.

With 80% of the U.S. self-storage market consisting of smaller regional and local owners, Public Storage looks primed to continue consolidating the industry through mergers and acquisitions (M&A) for decades to come. As evidenced by Public Storage’s high cash ROIC, its management has proven skillful at growing through M&A and has no shortage of funding thanks to its best-in-class credit ratings.

Since 2019, Public Storage has grown the square footage in its self-storage portfolio by 36% (adding twice as much square footage as its next-highest peer). Thus, Public Storage’s investments should (literally) pay dividends once the cyclical industry returns to sunnier days.

3. A higher-than-average 4.1% dividend yield

While the company doesn’t emphasize raising its dividend every year, its dividend payments have grown more than sixfold over the last two decades. This increase is good for 10% annualized growth. Even better, Public Storage’s current dividend yield is about 20% above its 10-year average.

PSA Dividend Yield data by YCharts

This 4.1% dividend yield, combined with the company’s expansion potential, offers investors the rare combination of high-yield payouts and sales growth.

4. A discounted valuation after a 30% drop in share price

Even with Public Storage’s industry-leading qualities and growth prospects, the company doesn’t trade at much of a premium valuation when compared to its peers.

PSA Price to CFO Per Share (TTM) data by YCharts

Not only is Public Storage’s valuation broadly in line with that of its two more profitable peers, but at 17 times cash from operations (CFO), it is near a decade-long low.

Altogether, this discounted valuation, paired with the company’s 4.1% dividend yield, enticing growth prospects, and best-in-class operations, make Public Storage one of my favorite S&P 500 dividend stocks to buy in 2025 and hold forever.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.