Our Terms & Conditions | Our Privacy Policy

- Package developed in collaboration with CBSL, SLBA, SME sector representatives, and relevant government agencies

- Assures the measures were prepared with a long-term perspective to provide breathing space for affected SMEs while ensuring the stability of the banking sector

- SMEs that obtained credit facilities from a licensed bank classified as stage 3 (on or after 1. 4.2019, and those commencing discussions with the respective Relief Banking Unit on or before 31.3.2025, are eligible for the package

Sri Lanka’s struggling businesses can find some respite as the Finance Ministry yesterday announced details of a relief package for small and medium-sized enterprises (SMEs) facing difficulties servicing their debt due to the economic crisis following the global health pandemic.

The package was developed in collaboration with the Central Bank of Sri Lanka (CBSL), the Sri Lanka Banks’ Association, SME sector representatives, and relevant government agencies.

The Finance Ministry assured that the measures were prepared with a long-term perspective to provide breathing space for affected SMEs while ensuring the stability of the banking sector.

Accordingly, SMEs that obtained credit facilities from a licensed bank classified as stage 3 (non-performing loans – NPLs) on or after April 1, 2019, and those commencing discussions with the respective Relief Banking Unit on or before March 31, 2025, are eligible for the package, subject to submission of all required documents.

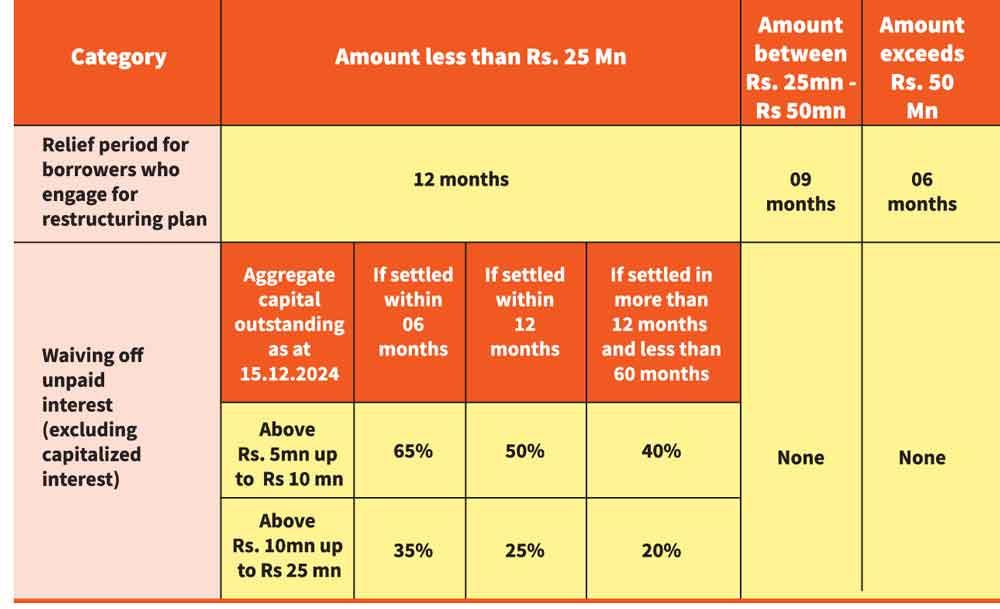

Specific relief measures have been proposed under three categories based on the aggregate capital outstanding of credit facilities as of December 15, 2024.

Under general relief, the commencement of legal action is extended until March 31, 2025, allowing SMEs to enter a revival plan by amending the Recovery Loans by Banks (Special Provisions) Act No. 4 of 1990.

If required, eligible SMEs may be granted a working capital loan, subject to repayment capacity and the submission of a credible business revival plan on a case-by-case basis to re-boost them to their pre-crisis operating status.

An adverse Credit Information Bureau (CRIB) report shall not be the sole reason for declining loan applications from eligible borrowers. Licensed banks, in consultation with the CRIB, may develop an appropriate reporting modality for restructured credit facilities under this relief. Furthermore, SMEs may request a breakdown of the capital, interest, and other charges of their credit facilities from their bank.

In addition to the specific and general relief measures, the Finance Ministry has requested the CBSL to explore the possibility of incorporating a few additional measures to the package to ensure smooth implementation and maximum benefit to the SME sector.

The first is the introduction of a reasonable interest rate for restructured loans below Rs. 50 million, subject to a maximum of the Average Weighted Prime Lending Rate (AWPR) plus a reasonable margin.

The second is for the maximum loan repayment period to be 10 years (unless the original agreement provided a longer period), subject to a grievance handling process for aggrieved parties.

The third is to rename “Business Revival Units” of the respective banks as “Relief Banking Units.”

Furthermore, all legal actions are to be suspended for cases during the proposed relief period: 12 months for loans below Rs. 25 million, nine months for loans between Rs. 25 million and Rs. 50 million, and six months for loans above Rs. 50 million, including a complete freeze on legal proceedings related to NPL loans in the relevant categories, except for dates already scheduled.

Lastly, a transparent mechanism is to be established for grievance handling in the event of a dispute over the valuation for auctioning a property between banks and the defaulter, ensuring the borrower’s property is auctioned at the highest possible rate to maximize its value.

Meanwhile, as additional policy measures to assist the SME sector, the Ministry of Finance called for the establishment of an advisory committee for SMEs under the leadership of the Ministry of Industries as a prime arm for SME policy development. This committee will provide guidance and coordinate the work of all relevant stakeholders under different institutions for SME sector development, bringing them under one umbrella.

It also urged the need to introduce a scorecard/rating mechanism in collaboration with the Institute of Chartered Accountants of Sri Lanka (ICASL) and other professional accounting bodies to support SMEs in increasing their ability to access finance.

Lastly, it suggested providing backup support by offering credit guarantees for bank loans of SMEs, alleviating collateral issues in obtaining bank loans in collaboration with the National Credit Guarantee Institution Limited (NCGIL), which is scheduled to commence operations from January 2025.

For the period of April 1, 2019, to September 30, 2024, approximately 494,000 loans amounting to Rs. 886 billion have been classified as stage 3 loans (NPLs) in the banking industry. It is noted that 99 percent of the number of loans categorised under stage 3 are below Rs. 25 million.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.