Our Terms & Conditions | Our Privacy Policy

Follow the money! Datacentre M&A hit $57bn in 2024, Digital Platforms and Services

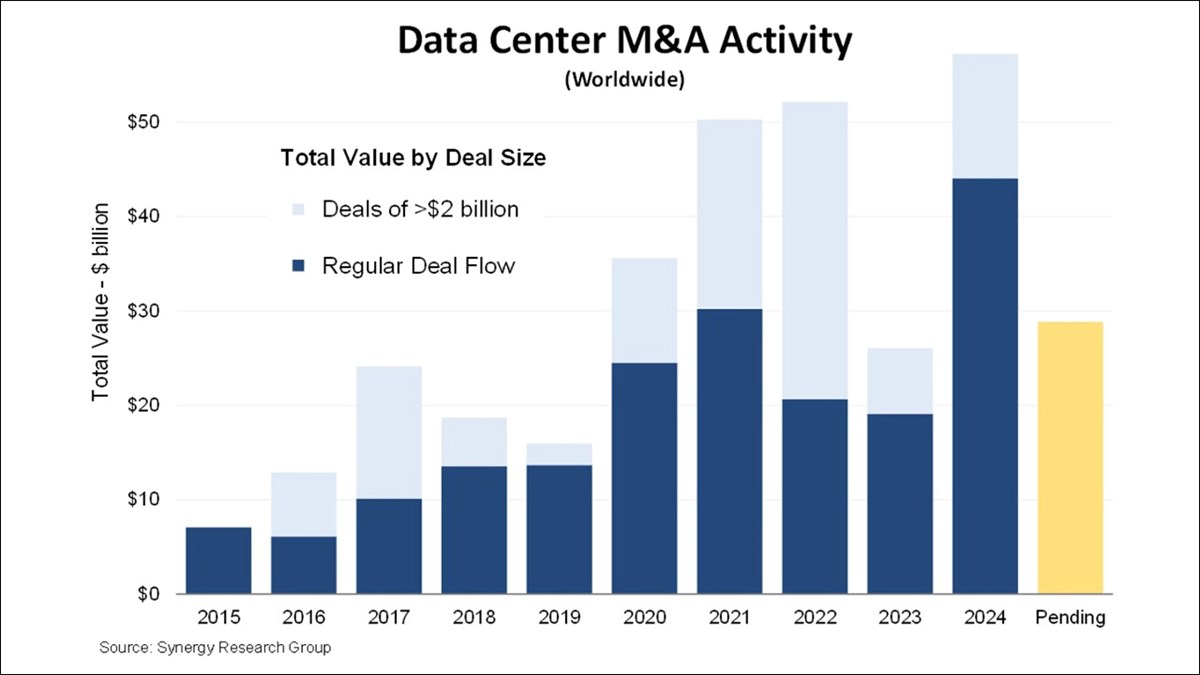

With AI now driving much of the world’s enterprise transformation plans and digital strategies, billions of dollars are being poured into the construction and acquisition of the datacentre facilities that are needed to support cloud and AI workloads, with the value of datacentre-oriented merger and acquisition (M&A) deals that closed in 2024 totalling $57bn, according to Synergy Research Group, topping the $52bn worth of deals that closed in 2022.

“There has been a tremendous increase in the demand for datacentre capacity, driven by cloud services, social networking and a range of both consumer and enterprise digital services,” noted John Dinsdale, a chief analyst at Synergy Research Group.

“There is no end in sight to this trend, with generative AI technology and services adding a further boost to already strong demand. Specialist datacentre operators have either not been able or were not prepared to fund those investments themselves, while private equity investors have been more than willing to step in and fund growth initiatives. Looking at pending deals and the future pipeline, there is plenty of evidence to suggest that 2025 will be another boom year for datacentre M&A,” added the analyst.

That’s because there is another $29bn worth of M&A deals already underway that have not yet closed, and Dinsdale and his team have identified “a pipeline of well over $15bn in possible future deals, where companies are seeking new sources of funding or considering strategic options.”

According to Synergy Research, the biggest deals to close in 2024 were two separate equity investments in Vantage Data Centers which, when combined, were worth $9.2bn: Vantage also received equity investments in its EMEA operations worth a total of $3.1bn.

But was there one even bigger that snuck in just before the end of year and, perhaps, not included in the Synergy Research total for last year? Investment firm Blackstone concluded the AUS$24bn (US$14.8bn) acquisition of Asia Pacific datacentre operator AirTrunk on 23 December, with the companies claiming it was the “largest ever datacentre deal globally”. If that deal makes the cut – and it looks like it does – then the total for 2024 would top $70bn.

The Synergy Research team carves the datacentre M&A market into “megadeals” worth more than $2bn and “regular” deals worth less than that threshold. As the chart above shows, 2021 was dominated by such regular deals, while 2022 saw fewer but was topped up by megadeals, including two that were valued at more than $11bn each – the $15bn acquisition of CyrusOne by private equity firms KKR and GIP, and the $11bn acquisition of Switch by DigitalBridge and IFM Investors. Then 2023 saw a lull in activity across the board before the $57bn worth of deals that were completed last year, the vast majority of which were “regular”

Since 2015, Synergy Research has logged 1,498 datacentre-oriented M&A deals worldwide, worth on aggregate about $300bn: Most of the activity comprises company acquisitions, but the totals also include minority equity investments, investments in joint ventures, acquisitions of individual datacentres, share sales and acquisition of land for datacentre development.

– Ray Le Maistre, Editorial Director, TelecomTV

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.