Our Terms & Conditions | Our Privacy Policy

As India expands its digital economy and accelerates its push for financial inclusion, will its legacy banks and financial institutions gradually lose their relevance as lending leviathans? Home to 1.4 Bn and on track to emerge as a $5 Tn economy by the end of this decade, the country has already seen a massive adoption of digital payment systems and financial services. The fintech market opportunity is estimated to reach more than $2.1 Tn by 2030, with digital lending projected to account for 60% of that market, surpassing $1.3 Tn.

However, the reality is not as hunky-dory as one would like. According to the RBI data, the Financial Inclusion Index rose to 64.2 in FY24 from 60.1 the previous fiscal year, leaving a significant portion of the population unserved and underserved. In addition, the central bank’s regulatory clampdown to curb lenders’ overexuberance will likely raise the cost of capital and hurt potential borrowers lacking documentation and/or a formal credit history.

Banks and FIs are increasingly working with fintech startups and third-party solutions to broaden access to essential financial services like credit, neobanking and open banking. But this multi-party banking ecosystem, or banking-as-a-service (BaaS), is inadequate for bridging the digital finance divide. The reason? Regulatory hurdles and technical setbacks often obstruct seamless operations, slowing the service spread in critical areas like lending.

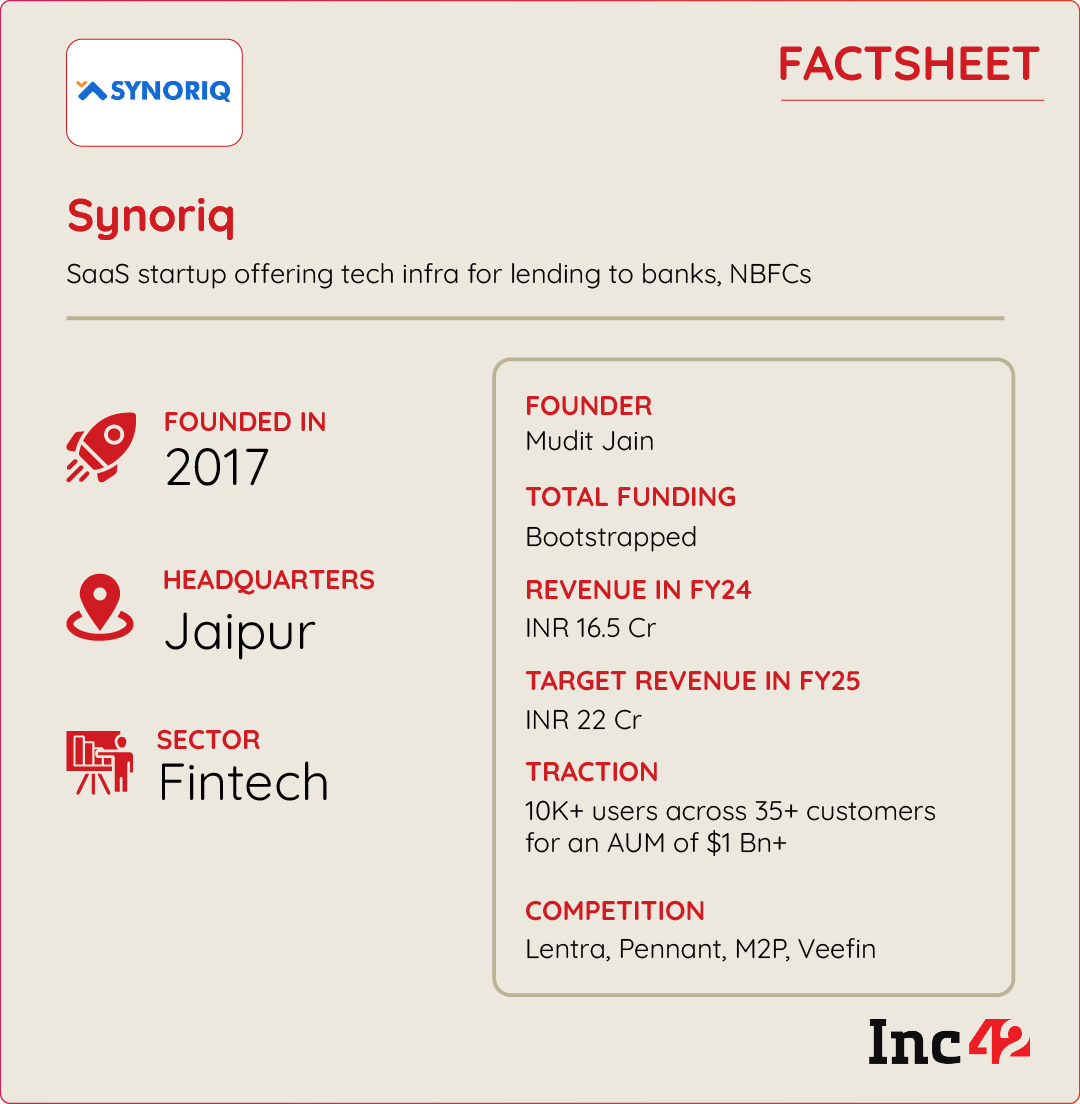

Mudit Jain, a B.Tech from IIT-Bombay, realised this when he launched Synoriq as a technology consultation and business advisory for banks, NBFCs and fintechs. He started as an edtech entrepreneur but soon moved to what he knew best – developing technology solutions for new and legacy financial institutions. However, his project ideas for inclusive growth often hit a roadblock as core banking systems were entrenched in legacy tech and failed to keep pace with fast-evolving requirements.

“To ride a Ferrari, we need better roads first. So, we started building high-quality lendingtech infrastructure as an alternative to legacy systems. As traditional lending rapidly transforms into a technology-driven business, banks and FIs need new-age technology for quick execution, fast growth and better control at lower operating costs,” Jain told Inc42.

Synoriq has developed an easily configurable, single-code SaaS product that combines loan origination system (LOS), loan management system (LMS), collection and customer service into a seamless platform capable of supporting innovation at scale. Think of the core lending infrastructure as an ERP system that lenders can use to run their operations efficiently. Once the software is deployed and integrated at the backend, it can manage the entire loan lifecycle and support 15+ products including personal and commercial loans.

The bootstrapped venture is backed by iStart, the Rajasthan government’s flagship initiative to boost the state’s startup ecosystem (more on that later). It claims a 70% rise in customer base as a fintech product firm just 2.5 years into its journey (earlier, it was a consultancy) and eyes a 60% CAGR in the next five years leading to an IPO. Synoriq has adopted a pay-as-you-grow subscription model, aims to achieve a 33.3% jump in revenue in the current financial year and looks to raise a Series A round.

How Synoriq Built A World-Class Alternative To Legacy Lending Management

From his IIT days, Jain had a passion for innovation and an entrepreneurial drive. As the India head of FinMechanics, a Singapore-based enterprise IT platform bridging capital markets and cloud strategies, he collaborated closely with several private-sector banks and saw an opportunity to disrupt outdated legacy systems. The turning point came when Synoriq finally shifted its focus, pivoting from an advisory role to building the dynamic, configurable lendingtech infrastructure.

“Synoriq stands for synergy with quest – a constant quest for excellence,” the founder and CEO said. “However, we underestimated the complexity of creating a comprehensive platform fit to run end-to-end lendingtech operations.”

The startup scaled its customer base too rapidly without going through product iteration and refinement, leading to a wave of negative feedback. In response, the business spent an entire year perfecting the product and prioritising customer satisfaction over fast-paced expansion. “The year-long focus on building a premium product has given us a much-needed technology edge over competition and underlined our commitment to customer support,” said Jain.

Despite these twists and turns, the founder claimed profitability from the beginning, and those extra bucks from its consultancy business helped meet its development and operational costs when Synoriq changed tack. That is how the new avatar has gone forward without investor dollars and may soon become fully sustainable.

span {

margin: 0;

padding: 3px 8px !important;

font-size: 10px !important;

line-height: 20px !important;

border-radius: 4px !important;

font-weight: 400 !important;

font-style: normal;

font-family: noto sans, sans-serif;

color: #fff;

letter-spacing: 0 !important;

}

.code-block.code-block-55 .tagged {

margin: -4px 0 1px;

padding: 0;

line-height: normal;

}

@media only screen and (max-width: 767px){

.code-block.code-block-55 {

padding:20px 10px;

}

.code-block.code-block-55 .recomended-title {

font-size: 16px;

line-height: 20px;

margin-bottom: 10px;

}

.code-block.code-block-55 .card-content {

padding: 10px !important;

}

.code-block.code-block-55 {

border-radius: 12px;

padding-bottom: 0;

}

.large-4.medium-4.small-6.column {

padding: 3px;

}

.code-block.code-block-55 .card-wrapper.common-card figure img {

width: 100%;

min-height: 120px !important;

max-height: 120px !important;

object-fit: cover;

}

.code-block.code-block-55 .card-wrapper .taxonomy-wrap .post-category {

padding: 0px 5px !important;

font-size: 8px !important;

height: auto !important;

line-height:15px;

}

.single .code-block.code-block-55 .entry-title.recommended-block-head a {

font-size: 10px !important;

line-height: 12px !important;

}

.code-block.code-block-55 .card-wrapper.common-card .meta-wrapper .meta .author a, .card-wrapper.common-card .meta-wrapper span {

font-size: 8px;

}

.code-block.code-block-55 .row.recomended-slider {

overflow-x: auto;

flex-wrap: nowrap;

padding-bottom: 20px

}

.code-block.code-block-55 .type-post .card-wrapper .card-content .entry-title.recommended-block-head {

line-height: 14px !important;

margin: 5px 0 10px !important;

}

.code-block.code-block-55 .card-wrapper.common-card .meta-wrapper span {

font-size: 6px;

margin: 0;

}

.code-block.code-block-55 .large-4.medium-4.small-6.column {

max-width: 48%;

}

.code-block.code-block-55 .sponsor-tag-v2>span {

padding: 2px 5px !important;

font-size: 8px !important;

font-weight: 400;

border-radius: 4px;

font-weight: 400;

font-style: normal;

font-family: noto sans, sans-serif;

color: #fff;

letter-spacing: 0;

height: auto !important;

}

.code-block.code-block-55 .tagged {

margin: 0 0 -4px;

line-height: 22px;

padding: 0;

}

.code-block.code-block-55 a.sponsor-tag-v2 {

margin: 0;

}

}

]]>

Here is a quick look at Synoriq’s five standout features, which set it apart.

An evolutionary architecture: Synoriq’s unique selling point is its ‘evolutionary architecture’, a flexible, security-driven and scalable infrastructure solution that ensures lenders can meet changing market demands. The startup offers a configurable system with a strong focus on customer support. It is a dynamic and evolving offering that constantly learns and adapts to ensure lendingtech operations remain resilient and future-ready.

A feature-rich platform: The feature-rich platform is designed to stay ahead of industry trends, offering superior configuration, seamless integration and stringent security. Its all-encompassing lendingtech infra suite can address every requirement, from customer onboarding to credit underwriting, disbursement, collection and support across loan categories such as home loan, vehicle loan, gold loan, education loan, agri loan, term loan, credit line, co-lending, subvention and more.

Innovative but secure and reliable: Synoriq combines new-age capabilities with the stability and maturity of legacy systems. For large lenders looking for sturdy and scalable infrastructure, the startup offers modern solutions without compromising reliability. “Our highly secure and robust infrastructure effortlessly scales to handle any loan volume, empowering lenders to grow without boundaries,” said Jain.

Laser focus on compliance: Compliance has been a longstanding pain point for lendingtech startups and legacy FIs. Synoriq constantly monitors the ever-shifting regulatory landscape to ensure businesses can easily navigate complexities.

World-class customer satisfaction: After the initial setback, Synoriq’s journey now revolves around achieving world-class customer satisfaction, aiming to set new benchmarks for Net Promoter Score (NPS) in the lending software industry. For context, NPS is a critical metric used to measure customers’ likelihood to recommend a company’s products or services, underscoring customer satisfaction (CSAT) and loyalty. Jain said a rapid growth phase would be on the cards after achieving a super-high CSAT.

When iStart Rajasthan Catalysed Synoriq’s Growth

Ask Jain why he set up headquarters in Jaipur instead of India’s Silicon Valley (Bengaluru) or its commercial capital (Mumbai), and he comes up with a unique response. “I believe talent is equally distributed [you can set up a good team almost anywhere in the country], but opportunities are not. Hence, I decided to start a world-class company in Jaipur with active handholding from iStart Rajasthan.”

The state government runs the initiative to promote local startups, new investments and job creation. For instance, the QRate programme under iStart assessed Synoriq’s business concept in the first place, bolstering the team’s confidence to pivot and scale. Regular mentoring, networking opportunities with prospects and high-impact events also played a pivotal role in driving the startup’s growth.

“iStart gave us the confidence to dream big. It consistently mentored and advised us, organised useful events and connected us to prospects and investors. The Rajasthan government did a great job when it launched the initiative and opened up a new era in supporting startups across the state,” said Jain.

Can Synoriq Transform The Tech Backbone Of Digital Lending?

Lending in India is rapidly emerging as a more regulated and organised sector driven by key policy interventions, including the Draft Bill called BULA (Banning of Unregulated Lending Activities) and the RBI’s Digital Lending Guidelines for regulated entities. As compliance becomes paramount, there will be rising demand for precise data analytics to validate credit profiles, simplified and cost-effective portfolio management through automation and enhanced customer satisfaction at every interaction point. Given this scenario, the loan servicing software market is poised to grow exponentially.

Globally, the loan management software market is estimated to reach $29.9 Bn by 2031 from $5.9 Bn in 2021. Although India’s numbers are not immediately available, there has been significant credit growth in the post-pandemic years, and the software market will grow accordingly. For instance, India’s alternative lending market is expected to grow by 17.7% annually during 2024-28 to reach $18.2 Bn.

Recognising this market’s potential, Synoriq focuses on enhancing customer satisfaction, pushing its SaaS solutions across markets and looking for higher referral rates. In the long term, it aspires to emerge as an industry trailblazer, delivering state-of-the-art infrastructure solutions for lendingtech operations.

As the lending sector continues to expand, the technological infrastructure supporting the flow of billions of dollars must be robust, innovative and highly accessible. The lending businesses seek backends that can effectively adapt to, comprehend, and address modern challenges.

More importantly, using GenAI will also play a critical role. According to Fortune Business Insights, a 2024 Fannie Mae Mortgage Lender Sentiment Survey revealed that 73% of lenders valued the tech for enhancing operational efficiency and found that compliance reviews and customised mortgage loans were GenAI’s most compelling use cases.

Synoriq and its peers are already pushing the boundaries of innovation to future-proof lendingtech. However, integrating GenAI with loan servicing software is bound to enhance their tech impact due to sharper decision-making, optimised portfolios and improved operational efficiency. How fast these Indian startups can adopt global technology trends will determine their growth.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.