Our Terms & Conditions | Our Privacy Policy

The digital wallet landscape is undergoing a profound transformation, evolving far beyond its initial role as a tool for electronic payments.

As technology, regulation and consumer expectations shift, digital wallets are emerging as comprehensive financial platforms that integrate payments, identity verification and asset management.

The Mobey Forum’s latest report, Beyond Payments: Navigating the Next Generation of Digital Wallets, provides an in-depth analysis of this evolution, offering critical insights for financial institutions, fintech firms and payment service providers.

Digital Wallets: A New Definition for a New Era

The rapid expansion of wallets demands a new conceptual framework.

Traditionally, wallets were seen merely as digital versions of physical wallets, focused on storing card details and facilitating transactions.

However, the Mobey Forum proposes a broader definition: A digital wallet is an interface to interact with and manage verified data and digitised assets securely.

This redefinition reflects the wallet’s growing role in managing digital identity, electronic documents and even digital assets like cryptocurrencies and tokenized securities.

The Changing Landscape of Digital Wallets

From Payment-Focused to Multi-Asset Wallets

The initial wave of wallets, spearheaded by Apple Pay and Google Pay, focused primarily on enabling seamless card-based transactions through mobile devices.

While these solutions have seen widespread adoption, they still rely on traditional card infrastructure, offering little room for innovation beyond contactless payments.

The next generation of wallets is shifting toward bank account-centric solutions, leveraging real-time payment systems like UPI in India and PIX in Brazil.

By bypassing traditional card networks, these wallets reduce transaction costs and offer instant, direct transfers between accounts.

The recent launch of Wero, the European Payments Initiative’s digital wallet, signals Europe’s move toward a similar model.

The Diversification of Digital Wallets

Digital wallets are no longer confined to payments. The Mobey Forum report identifies six emerging categories of wallets:

-

Merchant Wallets – Businesses are increasingly adopting wallets for integrated commerce solutions, allowing seamless checkout, loyalty programs and personalised marketing.

-

Transit Ticketing Wallets – Wallets are being integrated into urban transportation systems, enabling digital ticketing for metros, buses and even ride-sharing services.

-

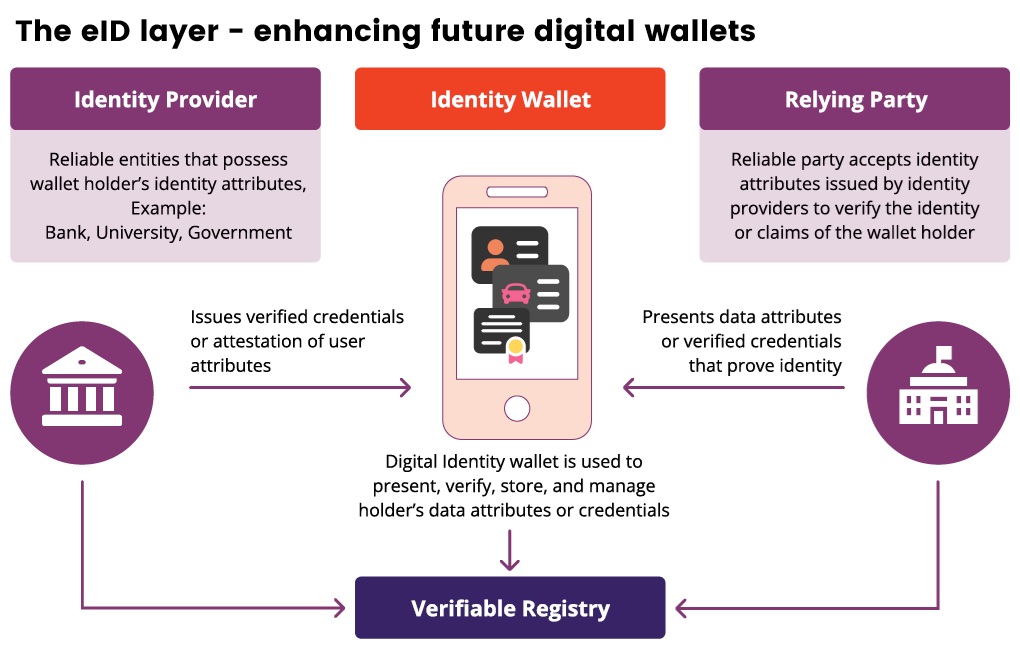

eID Wallets – With the rise of electronic identity (eID), digital wallets are being used for secure identity verification, digital signatures and online authentication.

-

Digital Asset Wallets – As blockchain-based assets grow, wallets are adapting to store and manage cryptocurrencies, NFTs, and tokenized securities.

-

P2P Wallets (Local Champions) – Regional solutions such as Swish (Sweden), Twint (Switzerland), and Bizum (Spain) are thriving by providing instant, fee-free peer-to-peer payments.

-

Super App Wallets – In Asia, wallets like Alipay and WeChat Pay are evolving into multi-functional platforms that combine payments, banking, e-commerce, and lifestyle services.

The Future of Wallets: eID-Enabled Asset-Centric Platforms

The next frontier for digital wallets lies in secure identity management.

Governments worldwide are recognising the need for secure, interoperable digital IDs and digital wallets are becoming the preferred tool for managing these credentials.

The European Union’s eIDAS 2.0 regulation mandates that all EU member states offer digital identity wallets to citizens by 2026, enabling secure access to public and private services.

These wallets will store verified credentials, including passports, driver’s licenses and financial data, fundamentally changing the way identity verification works online.

Open Banking and Embedded Finance Driving Wallet Innovation

The rise of Open Banking and Embedded Finance is accelerating digital wallet adoption.

These trends enable wallets to integrate with a broader financial ecosystem, offering users seamless access to banking, lending, insurance and investment services within a single interface.

Banks and fintechs face a strategic decision: Should they build their own digital wallets or collaborate with third-party providers?

The Mobey Forum suggests three key strategic considerations for banks:

- Local Champions and eID Wallets – Banks can leverage their regulatory expertise and consumer trust to develop secure, bank-backed wallets.

- Open Finance as a Growth Strategy – By integrating financial services into digital wallets, banks can enhance customer engagement and create new revenue streams.

- Interoperability and Partnerships – Financial institutions must prioritise interoperability to ensure seamless integration across different ecosystems.

Challenges and Opportunities for Banks

While wallets present a significant opportunity, banks must overcome several challenges:

- Consumer Trust – Concerns about data privacy, security and centralisation remain high, particularly around CBDCs and government-backed identity wallets.

- Regulatory Compliance – Wallets must comply with evolving financial regulations, including PSD2 in Europe and data protection laws like GDPR.

- Competition from Big Tech – Tech giants like Apple, Google and Meta are aggressively expanding their payment ecosystems, posing a threat to traditional banks.

Strategic Recommendations

The Mobey Forum urges financial institutions to act decisively to remain competitive. Key recommendations include:

- Develop a clear wallet strategy – Banks must define their role in the wallet ecosystem and align their offerings with consumer expectations.

- Embrace collaboration – Rather than competing with fintechs, banks should explore partnerships to enhance wallet capabilities.

- Focus on consumer needs – Security, privacy and seamless user experience should be top priorities.

The fact is, digital wallets are no longer just about payments – they are becoming, as was predicted, comprehensive financial platforms that integrate identity, banking and digital assets.

With the rise of eID, Open Banking and embedded finance, the next generation of wallets will redefine how consumers interact with financial services.

For banks, fintechs, and payment providers, the key to success lies in embracing innovation, fostering strategic partnerships and prioritising consumer trust.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.