Our Terms & Conditions | Our Privacy Policy

Among the real estate players that witnessed excellent turnaround in their fortunes in the post-Covid residential and commercial construction boom from FY21, Anant Raj was a prominent beneficiary. A major additional driver for the stock was the company’s foray into the data centre business, though the segment itself is yet to contribute significantly to overall revenues.

After a relentless run, the stock is down over 50 per cent from its recent peak in January. While the correction in the broader markets triggered by FPI selling, corporate earnings weakness and US trade tariff challenges led to an up to 25 per cent correction in mid- and small-cap indices, some stocks in this space suffered a lot more.

There was also excessive pessimism on the prospects of the nascent cloud/storage business of the company after the DeepSeek AI announcement led to fears that data centre capex the world over would face a reduction (this aspect will be discussed later).

At ₹450, the stock trades at 25 times its per share earnings for FY26, making it a reasonable bet for investors with a two-three-year perspective, especially given the elevated valuations that most of the relatively-larger real estate companies trade at currently. The BSE Realty trades at a PE multiple of over 48 times.

Robust traction in its residential construction business spanning luxury and affordable segments, visibility in its commercial division and healthy demand in its data centre offering, expected to start contributing to revenues significantly in the coming two-three years, are positive factors.

The company also has a healthy balance sheet with very insignificant net debt levels.

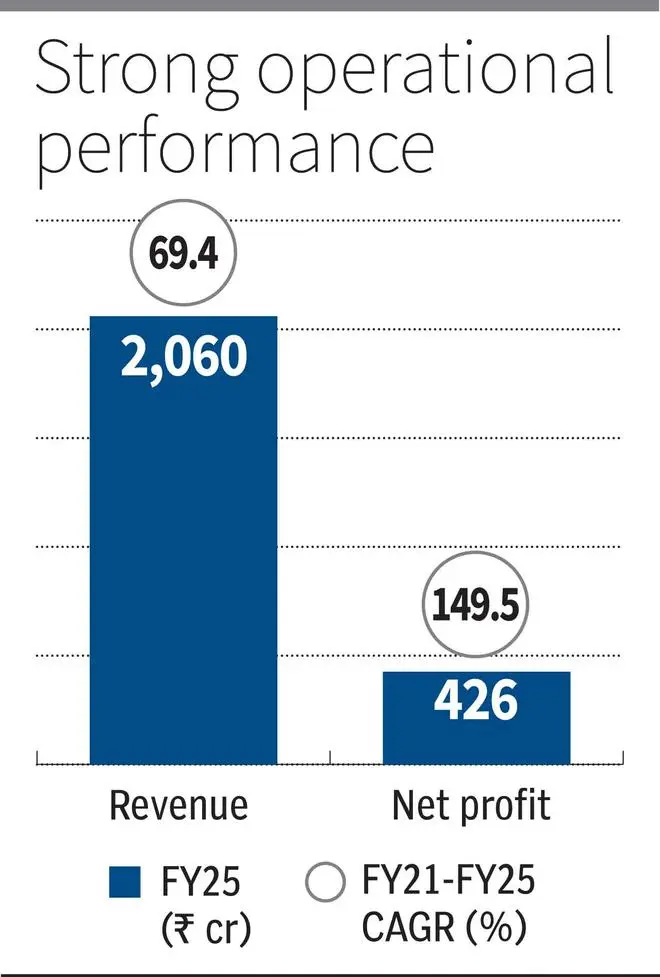

Over FY21-25, Anant Raj’s revenues grew at 69.4 per cent compounded annually to ₹2,060 crore, while net profits rose at 149.5 per cent to ₹426 crore in FY25. Revenue grew at 38.9 per cent and net profit expanded at 60.1 per cent year on year in FY25.

Multiple real estate levers

The firm is largely a real estate player focused on the NCR region (mostly in Gurugram). Residential luxury projects, group housing, affordable housing (in Tirupati), plots and villas are areas that it specialises in.

There are projects spanning 220 acres of integrated development in Gurugram. About 10.87 million sq ft of ongoing and planned projects are on the horizon, with a total expected revenue of ₹22,000 crore over the next several years.

Since it operates in a high-end area of Gurugram, realisations on residential projects are high. In its group housing project, for example, the average selling price is ₹18,000 per sq ft.

Anant Raj also has a commercial spaces segment spanning hotels, IT parks and office spaces. These businesses have steady rental income visibility for the foreseeable future.

Data centres coming on stream

Anant Raj has been providing co-location services since 2019. In recent years, it has also started offering cloud services (infrastructure as a service) in association with Orange Business. It intends to get into AI-enabled solutions as well.

By Q1FY26, the company expects as much as 28 MW of data centre capacity to be operational. Over the next five-odd years, it expects to have over 300 MW up and running.

Revenues from the segment are insignificant currently. However, after the 28 MW capacity gets operationalised, the data centre segment may contribute significantly (more than 10 per cent) of the revenues by FY26. Over the next two-three years, as more capacity comes on stream, about 25-30 per cent of the company’s revenues may be generated from the segment.

The key aspect to note here is that the data centre business generates an operating margin of 75 per cent or more. So, when more revenues flow in, company margins would expand.

Anant Raj mostly had public sector companies as clients in its data centre business thus far, but increasingly even private firms are seeking its cloud services.

Rising e-commerce usage, faster 5G rollout, cloud computing explosion and data protection law compliance are growth triggers for the company. AI and machine learning would be future drivers.

Anant Raj has the added advantage of having its own real estate to house data centres by virtue of its large land bank.

India’s data centre capacity crossed 1 GW in 2024, according to a recent report from JLL India, tripling from 2019-levels. Much of the capacity is absorbed. Another 795 MW is expected to be added over 2025-27. Average rents per kVA per month for a 5-20 MW capacity data centre are ₹7,000 in Mumbai. One MW is 1,000 kVA.

According to another Anarock Capital report, the Indian data centre industry is worth $10 billion currently and generated an estimated $1.2 billion for operators in 2023-24.

On DeepSeek’s entry reducing data centre requirements due to lower computational infrastructure requirements to train large language models, a recent report from Goldman Sachs provides clarity. It notes that questions remain on DeepSeek’s training, infrastructure and ability to scale. The report notes that AI-dedicated data centre is an emerging class of infrastructure and that very few exist currently. Global power demand from data centres will increase 50 per cent by 2027 and by as much as 165 per cent by the end of the decade (compared with 2023), as per Goldman Sachs Research estimates.

Further, recently-reported March quarter results and CY26 outlook from US Big Tech companies — Microsoft, Alphabet, Meta Platforms and Amazon also confirm this. Their CY26 mega capex plans related to AI data centre/cloud remains intact, as customer demand remains strong in this segment.

Strong financials

Anant Raj has been reducing debt in its balance sheet steadily over the past few years. In FY25, its net debt is just ₹50 crore and the net debt-to-equity ratio is insignificant.

The company enjoys a high EBITDA margin of 25 per cent and a net margin of over 20 per cent, which compares favourably among the best in the industry. Once the high-margin data centre business starts contributing significantly to the financials from FY26, margins would further head north.

Published on May 3, 2025

[ad_1]

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

[ad_2]

Comments are closed.