Our Terms & Conditions | Our Privacy Policy

Deals for insurance firms in US and Canada dip 15%, OPTIS Partners reports

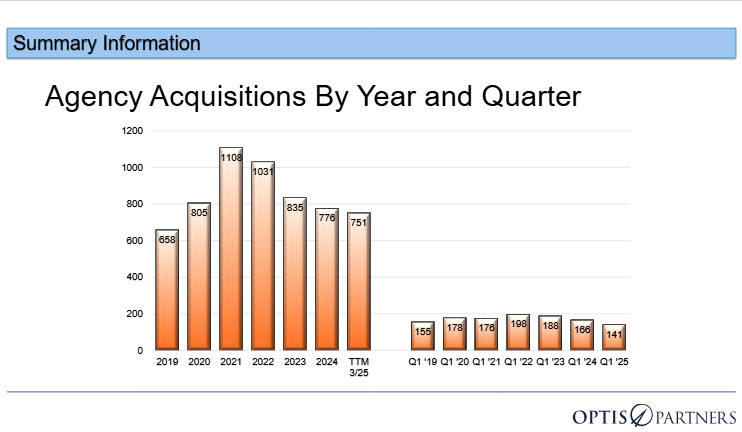

In what is being described as the slowest quarter since 2020, the total number of mergers and acquisitions nationally dipped 15% to 141 announced deals during the first quarter of 2025. The 141 announced insurance agency mergers and acquisitions represents a substantial drop from the 166 announced deals during the same period in 2024, according to OPTIS Partners’ M&A database. Q1-2025 also represents that ninth consecutive quarter to have fallen below the long-term trend line.

“We think the pace will ultimately pick up this year because of the large number of active buyers in the market, although current economic uncertainties may cause a bit of a delay,” said Steve Germundson, a partner at the Chicago-based investment banking and financial consulting firm that specializes in the insurance industry.

U.S. Agencies Dominate; Canadian Activity Modest

Of the 141 announced transactions in Q1, 139 involved U.S.-based agencies. The remaining six deals were for Canadian brokerages.

Massachusetts outpaces national average

The Commonwealth significantly outperformed the national average in insurance agency M&A activity during the first quarter of 2025, with eight announced transactions compared to the national per-state average of approximately 2.8 deals.

Based on OPTIS Partners’ tally of 139 U.S. agency sales for the quarter, Massachusetts recorded nearly three times the average number of deals, placing it among the most active states in the country. The elevated volume suggests a strong local appetite for consolidation, likely driven by a combination of active regional buyers and favorable market conditions for sellers in the Commonwealth.

Leading Buyers in Q1-2025

BroadStreet Partners led all buyers during the quarter with 18 transactions, followed by World Insurance Associates with 10 deals and King Insurance Partners with seven. Although Arthur J. Gallagher’s total transaction count was lower than usual, it announced two significant acquisitions: AssuredPartners (pending regulatory approval) and Woodruff-Sawyer.

Private Equity-Backed Firms Drive M&A

OPTIS tracks buyers across four categories: private equity-backed or hybrid brokers, privately held brokers, publicly traded brokers, and others. Private equity-backed or hybrid buyers continued to lead market activity, accounting for 73% of all Q1 deals—despite comprising only 26 active firms.

Privately held brokers completed 25 acquisitions during the quarter, while publicly held brokers announced 13.

P&C Agencies Account for Majority of Sellers

On the sell-side, property and casualty-focused agencies represented the majority, with 96 transactions, or 68% of the total. Employee benefits firms made up 11 deals (10%), and combination P&C/benefits agencies accounted for 14 (8%). The remaining 20 deals (14%) involved sellers categorized as “all others,” which includes TPAs, managing general agents, life insurance-focused firms, financial consulting agencies, and related entities.

Outlook: More Mega-Deals Expected in 2025

Looking ahead, the market may see a resurgence in deal activity, particularly among larger firms. “We also expect more large privately owned agencies will be sold this year,” said OPTIS managing partner Timothy J. Cunningham. “The sale of San Francisco-based Woodruff-Sawyer, with $268 million in estimated revenues, points to further mega-deals this year.”

Massachusetts also saw its first mega-deal of 2025 back in February with the announcement that Alera Group had acquired Kaplansky Insurance, one of the state’s largest privately held independent insurance agencies.

The full OPTIS Q1 2025 M&A report is available at: or by clicking the image below:

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.