Our Terms & Conditions | Our Privacy Policy

Paraguay banking in flux: Mergers, lower margins, and the challenge of optimization

The Paraguayan financial sector has been growing and strengthening over the last 20 years, according to Itaú Paraguay CEO José Britez, who offered his ideas on the changes within this sector and the country’s strategic areas for development.

“The balance has been very positive. There have been many investments in technology, which led to greater access to banking services across the entire financial sector. Regulations also facilitated this,” he told Herald sister publication Ámbito.

However, to sustain this growth, the banking sector must rethink its model, as intermediation margins are increasingly lower and new competitors are emerging in an economic context of growth.

In addition to new digital players such as Billetera Mango and Vaquita App (among others), non-traditional banks like Ueno Bank are expanding through technological innovation. Other traditional banks are also investing in technology for automated risk analysis. This is because the difference between lending rates (those charged for loans) and deposit rates (those paid to depositors) is increasingly narrow, leaving ever-decreasing gross margin for companies.

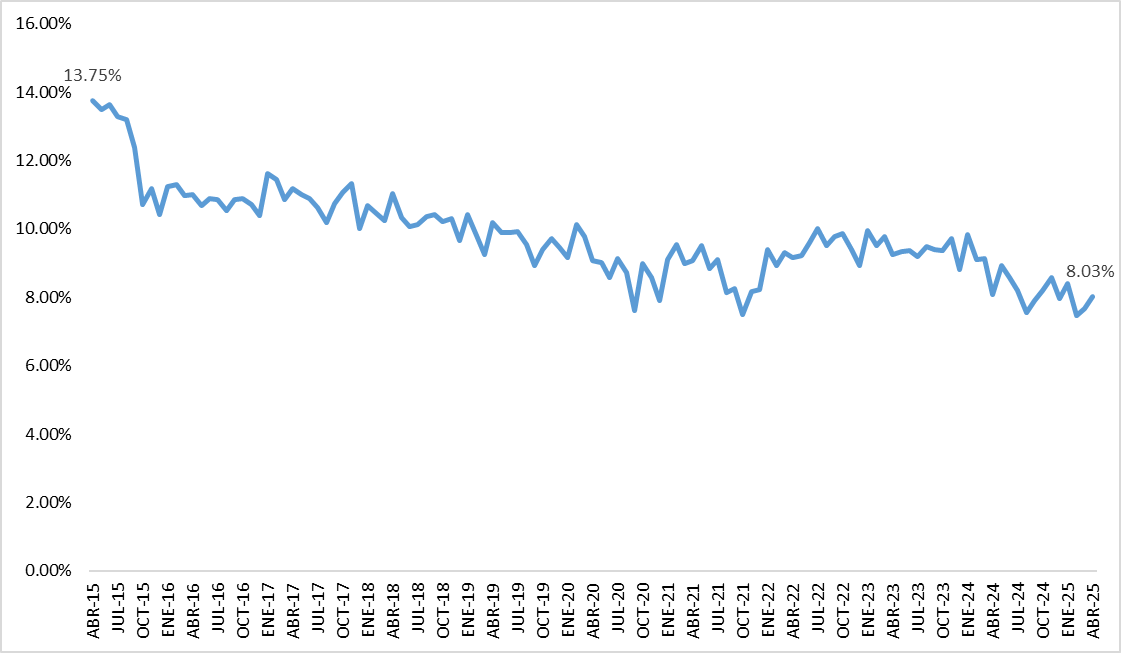

According to data from the Central Bank of Paraguay (BCP), the financial intermediation margin ten years ago was around 13.75%. With a clear downward trend over the last decade, it currently stands at 8%, 5.72 percentage points lower, with competition becoming increasingly more aggressive.

Caption: Evolution of intermediation margins in Paraguay’s financial sector (Data source: Central Bank of Paraguay.)

Mergers and acquisitions: Who are the market players?

Two traditional Paraguayan banks, Atlas and Familiar, are currently in the midst of a merging process. Banco Continental, one of the largest in the financial system, has already begun the process of absorbing Banco Río.

According to analysts and bankers, the reduction in intermediation margins is what’s causing business to shift from a margins-based model to one dependent on volume.

“It is normal for margins to narrow and commissions to become increasingly smaller due to competition and because new players are entering the market with lighter platforms and without the significant legacy that traditional banks have,” Britez explained.

According to the Itaú CEO, the biggest challenge is to change in order to continue growing “in quantity and quality of service, not price.”

The sector in numbers

Central Bank records show that bank loan portfolios closed in May 2025 at G$180.6 trillion (approximately US$22.7 billion), representing year-on-year growth of 21%. Deposit portfolios, meanwhile, grew by 12% in the same period, reaching G$174 trillion (close to US$22 billion).

This faster expansion of loan portfolios has become a trend in recent months. This reflects the current investment and consumption climate in the Paraguayan economy, which in turn has also contributed to competition between banks in terms of interest rates, both to attract savings and grant loans.

In terms of loan portfolio composition, the main player is the agricultural sector, accounting for 17% of the total with approximately G$31.3 trillion (just under US$4 billion), followed by the consumer portfolio (16%), and wholesale trade (15%). Although with smaller shares, the portfolios that have grown the most are real estate and services in general, at 39% and 35%, respectively.

Caption: Distribution of banking loans in Paraguay according to sector in May 2025 (Data source: Central Bank of Paraguay.)

In terms of profit ratios, the system currently has an ROA of 2.29% and an ROE of 20.82%. The banking system as a whole accumulated profits of G$2.2 trillion (approximately US$278 million) at the end of May 2025, a 9% increase compared to the previous year.

Bank loan delinquency has remained below 3% since June 2024, standing at 2.53% in May of this year.

Long-term credit: the missing link

The Paraguayan industry faces a structural problem: long-term credits. In a previous presentation, we outlined the structural problem the Paraguayan industry faces, in terms of the need for longer-term financing under development conditions. José Brítez agrees with this analysis, pointing out that this is precisely one of the main limitations for the aforementioned sectors.

“The truth is that, today, for large industries such as forestry or electro-intensive industries, there is no significant funding capable of providing solutions with the required terms and conditions. Not only in Paraguay, but throughout the world, this has had a different type of financing structure,” the executive acknowledged.

The solution, according to Brítez, would be an increase in state support. In fact, this is already being done through the Development Finance Agency (AFD, by its Spanish initials), a second-tier bank that is in the process of structuring products that will help industrial credit, such as a guarantee fund for the forestry sector.

“Today, there is no funding with the terms and conditions that this type of investment requires. This is not unique to Paraguay. In Brazil, for example, the BNDES (Brazilian Development Bank) was key to industrialization. Here, external capital and new financial structures will be needed,” he stated.

The Role of Paraguayan Banking in Economic Development

Through the binational hydroelectric plants Itaipu and Yacyretá, which Paraguay shares with Brazil and Argentina, the country has been supplied with renewable electricity for several decades. However, it is estimated that this quota will not be sufficient in the coming years, and therefore investments will be required in this sector.

In this context, when asked about the country’s strategic sectors for the future, Brítez pointed to the energy sector. By 2030, the projected increase in electricity demand will require urgent investments in generation, transmission, and distribution, and, in his opinion, this is no small feat.

“There is a tremendous opportunity in the electricity sector; it’s something immediate. Paraguay must invest in everything related to transmission, distribution, and new energy generation, in line with our vision that between 2030 and 2032 we will be consuming almost 100% of our traditional energy sources. Therefore, the energy sector will be extremely important,” Brítez commented.

He also highlighted the enormous potential of the forestry sector, which he described as “the ‘Paraguayan soybeans’ of the future,” referring to the importance this sector could have in the country’s exports and in attracting international capital. He cautioned, however, that long-term financing channels must be sought.

Along the same lines, he mentioned opportunities in the agro-industrial chain, logistics, urban infrastructure, and the electro-intensive industry, although he noted that many of these sectors still face a significant funding gap.

Capital markets as an ally

The capital market is rapidly expanding in the country. The largest banks, such as Itaú and Continental, are already entering this field through their own brokerage firms.

Given this reality, Britez emphasized the importance of the stock market as a natural complement to the financial system. He praised recent regulatory advances, such as the creation of the Superintendency of Securities (SIV), but recognized the need for clear rules and participatory construction processes.

“They are two complementary worlds. The capital market is the natural channel for financing the long-term investments the country needs,” he concluded.

Although still small compared to other countries in the region, the Paraguayan capital market is expanding rapidly. In the first half of 2025, trading on the Asunción Stock Exchange reached 27.2 trillion guarantors, equivalent to US$3.434 billion, representing a year-on-year growth of 25% compared to the same period last year.

Currently, Paraguay’s Gross Domestic Product (GDP) is estimated at approximately US$48.217 billion, according to the Central Bank of Paraguay. This means that the capital market represents approximately 15% of GDP, compared to just over 1% ten years ago. This represents significant progress, although there is still ample room for further growth.

The local market is predominantly fixed-income, as corporate and government bonds account for 98% of outstanding securities. However, other investment options, such as mutual funds and investment funds, are beginning to gain ground, while transactions like repurchase agreements are becoming more established.

As this is a market with longer terms than the traditional financial system, it acts as a useful complement to match maturities.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.