Our Terms & Conditions | Our Privacy Policy

【SMM Analysis】Looking Back at the High-Grade NPI Market in the First Half of 2025 H1— A Turbulent Journey on the Waves. Is It Expected to Ride the Winds and Break the Waves in the 2025 H2?

Navigating the High-Grade NPI Market in 2025 H1: A Rollercoaster Ride – SMM’s Analysis and Review:

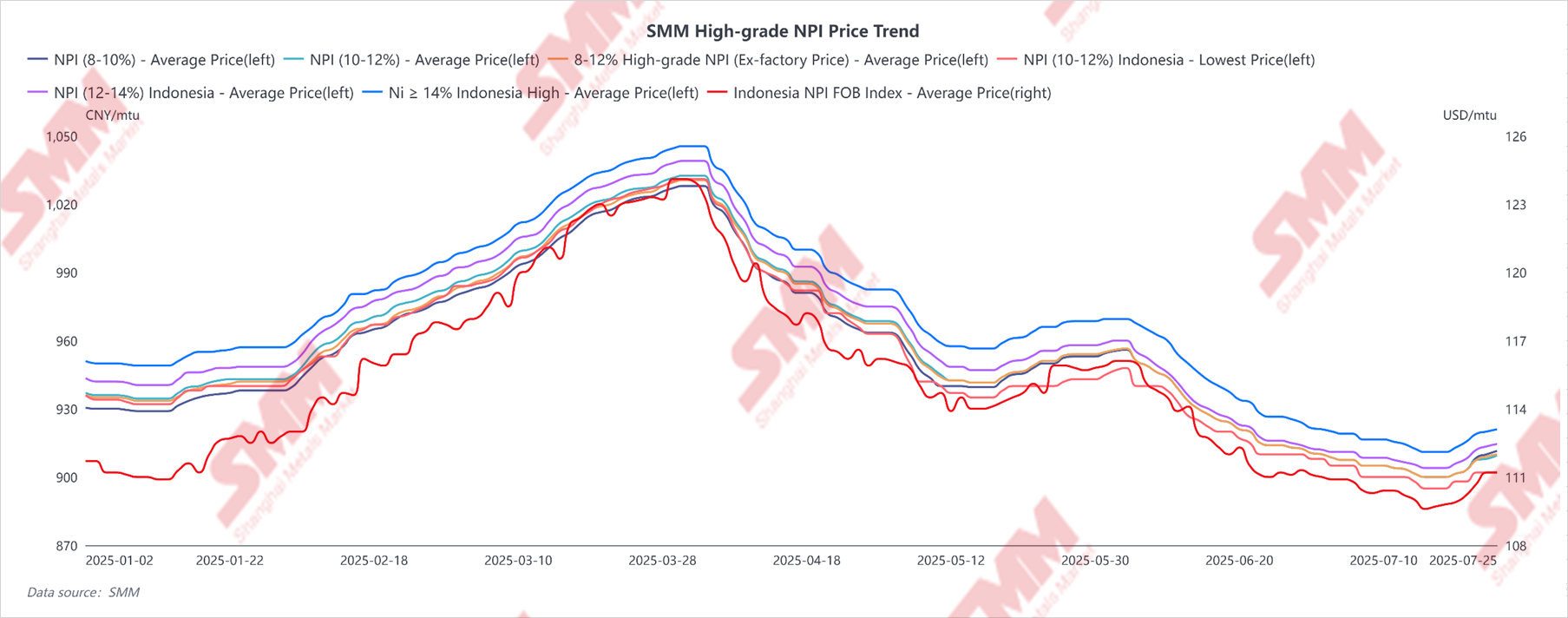

I. Review of High-Grade NPI Price Trends

In the first half of the year, the price trend of SMM’s high-grade NPI can be divided into two stages: the traditional positive feedback transmission in the industry chain during Q1, and the impact of the global tariff storm in Q2.

Q1 Overview:

Before the Chinese New Year, the transaction sentiment in the upstream and downstream of high-grade NPI was sluggish. Upstream top-tier smelters achieved profits, and with the release of new capacity, total production showed a growth momentum. The downstream stainless steel market gradually entered a pre-holiday state, with consumption stagnating for a short period. Additionally, steel mills had a relatively high proportion of long-term agreements for high-grade NPI, resulting in a weak willingness to stockpile. As stainless steel prices stopped falling and stabilized before the Chinese New Year, some traders had strong expectations for the market after the holiday, pushing up procurement prices and slightly raising the market center of high-grade NPI, which maintained around 940 yuan/mtu (on board, including tax).

After the Chinese New Year, due to the short-term recovery in stainless steel demand, stainless steel prices began to rise, and steel mill profits started to expand. Although the national stainless steel production in February was affected by a reduction in production days, there was no significant decline, maintaining a high level of demand for high-grade NPI. From the supply side, a top-tier enterprise in Indonesia experienced a sharp decline in production due to production management adjustments that month. The downstream stainless steel market, concerned about raw material supply, saw stainless steel futures and spot prices soar, driving the transaction price of high-grade NPI in the raw material market into an upward channel. Under the trend of expanding steel mill profits, national 300-series stainless steel production in March broke historical records, and steel mills’ demand for high-grade NPI also reached a historical high. With a significant improvement in the supply-demand balance in the short term, the market transaction price for spot orders once reached 1035 yuan/mtu (on board, including tax).

Entering Q2, during the Qingming Festival, a sudden tariff storm erupted between China and the US. From April 2 to April 10, the reciprocal tariff continued to escalate, with the US adjusting tariffs on China to 145% (including a 34% base tariff + 50% retaliatory tariff + 41% additional punitive tariff + 20% fentanyl tariff). China adjusted tariffs on the US to 125% (with some commodities reaching a comprehensive tariff rate of 49%-125% after adding the base tariff). Global commodity prices plummeted, with stainless steel futures prices falling to a recent low of 12,650 yuan/mt, a decline of 8.6%. Spot prices fell by 600 yuan/mt in the short term, a decline of 4.36%. At that time, stainless steel marginal losses expanded, and the negative feedback channel opened. The pessimistic expectations triggered by the tariff impact led to a pullback in the price of high-grade NPI in the raw material market from highs. On May 12, the joint statement of the China-US talks showed unexpectedly positive progress, with bilateral tariff rates significantly decreasing and a 90-day exemption period granted. The stainless steel market responded positively to trading signals, and the rebound in stainless steel futures and spot prices benefited the raw material market. Traders had strong expectations under the positive macroeconomic background, pushing up procurement prices and raising the market price center. As the end of Q2 approached, the stainless steel market entered the traditional consumption off-season, compounded by the US’s fluctuating tariff policies, leading to the emergence of a “weak reality, strong expectations” market scenario. Coupled with the solid fundamentals and market trends in Q1, both the imports of high-grade NPI and the nationwide stainless steel production reached record highs, resulting in a slow market digestion rate in Q2. With both volume and price of stainless steel falling, top-tier enterprises even relaxed their sales policies to “no price limits, no quantity limits.” The negative feedback loop in the stainless steel market persisted, and the price of high-grade NPI continued to decline. Overall, in Q2, the price of high-grade NPI fell by approximately 11.45%.

From the perspective of price spreads between different grades, from Q1 to Q2, the discount of 8-12% high-grade NPI (ex-factory price) compared to 10-14% Indonesian high-grade NPI (arriving at port, tax-included price) was greater than 5 yuan per mtu. The discount of 8-12% high-grade NPI (ex-factory price) compared to Ni≥14% Indonesian high-grade NPI (arriving at port, tax-included price) was greater than 15 yuan per mtu. The discount of 8-10% high-grade NPI (ex-factory price) compared to 10-12% high-grade NPI (ex-factory price) was greater than 5 yuan per mtu, and the discount of 10-12% Indonesian high-grade NPI (arriving at port, tax-included price) compared to 12-14% Indonesian high-grade NPI (arriving at port, tax-included price) was greater than 5 yuan per mtu.

Starting from the middle of Q2, the premiums and discounts between different grades began to narrow. The price of 8-10% high-grade NPI (ex-factory price) gradually reached parity with that of 10-12% high-grade NPI (ex-factory price), and the discount of 10-12% Indonesian high-grade NPI (arriving at port, tax-included price) compared to 12-14% Indonesian high-grade NPI (arriving at port, tax-included price) was less than 5 yuan per mtu. In Indonesia, due to the high nickel ore prices and selling prices falling below costs, smelters increased the nickel grade to control costs. The rise in the average grade led to a narrowing of the premium for high-grade NPI. Additionally, as the production of relatively lower-grade high-grade NPI was concentrated in some Chinese smelters, the high-grade NPI flowed back to China more intensively. Downstream industries urgently needed lower-grade high-grade NPI to adjust the nickel content in steel grades, driving up the selling price of lower-grade NPI.

II. High-grade NPI Supply Side

In Indonesia, Q1 production first increased and then decreased. The supply increment came from the release of new capacity on Obi Island and Halmahera Island. In February, leading smelters in Central Sulawesi faced management adjustments, with operating rates maintained at only around 30%. Coupled with a reduction in production days, production experienced a slight decline. In March, with the expansion of smelter production profits and the ramp-up of new capacity, production recovered MoM. Overall, in Q1, Indonesia’s cumulative production reached 418,900 mt Ni, up 17.6% YoY. In Q2, production gradually declined due to the high premium of Indonesian nickel ore upstream and the continuous drop in selling prices of high-grade NPI caused by negative feedback downstream. As smelters incurred losses, some enterprises entered the maintenance stage, leading to a decrease in production. Overall, in the first half of 2025 (2025H1), Indonesia’s cumulative production reached 840,500 mt Ni, up 16.6% YoY.

In China, Q1 production declined sharply, mainly due to the increase in nickel ore prices in the Philippines. From the perspective of the rainy season cycle, after the Chinese New Year, the positive feedback transmission channel for stainless steel opened up. Palawan and Surigao, the main producing areas in the Philippines, were still in the rainy season, while the downstream demand for ore from high-grade NPI was released in a short period of time. The increase in nickel ore prices in the Philippines led to deeper losses for domestic smelters, with the disadvantage of self-production by integrated stainless steel mills magnifying the decline in production. Some traditional smelters also reduced production during this period to control the extent of losses. Overall, in Q1, China’s cumulative production of high-grade NPI reached 57.77 thousand mt Ni, down 8% YoY. In Q2, production first stabilized and then declined. Due to the optimistic market expectations in the early stage and the breakthrough in downstream stainless steel production to a record high, some domestic smelters resumed maintenance and production capacity ramped up. However, as the negative feedback from stainless steel continued to ferment in the late Q2, the weak prices of raw materials led to an expansion of smelter losses and a further decrease in production. Overall, in the first half of 2025 (2025H1), China’s cumulative production reached 112.14 thousand mt Ni, down 9.9% YoY.

On the import side, due to the increase in high-grade NPI production in Indonesia, the theoretically exportable volume expanded compared to the previous period. In Q1, imports followed a trend of initial decrease followed by increase. Despite the reduction in the number of days in February, imports still reached 104,700 mt Ni, and in March, they hit a new high of 113,700 mt Ni. Overall in Q1, cumulative imports amounted to 327,200 mt Ni, up 21.2% YoY. In Q2, imports steadily increased. However, due to uncertainties in international trade and frequent rainfall in multiple regions of Indonesia, which partially hindered shipments, imports declined significantly in April. From the overall perspective of H1 2025, the cumulative import volume of high-grade NPI reached 643,700 mt Ni, up 25.5% YoY.

III. Demand Side for High-Grade NPI

In terms of stainless steel production, China’s stainless steel production continued to expand in Q1. From the perspective of the stainless steel market performance, the post-Chinese New Year market rally materialized as expected, coupled with supply disruptions in the raw material sector, leading to an upward correction in stainless steel spot prices. With the expansion of stainless steel mill profits, the market sentiment was bullish, driving up the production schedules of stainless steel mills. In March, the production of 300-series stainless steel reached 1.96 million mt, hitting a record high. Overall, in Q1, China’s cumulative production of 300-series stainless steel was 5.2005 million mt, up 11.43% YoY. “March delivered as expected, but April missed the mark.” In Q2, the market was impacted by the global tariff storm, coupled with stainless steel gradually entering the off-season for consumption. Social inventory of stainless steel built up significantly, and spot prices entered a downward trend. Amid continuous losses at stainless steel mills, production declined. Overall, in H1 2025, China’s cumulative production of 300-series stainless steel was 10.6905 million mt, up 10.36% YoY.

In terms of demand for high-grade NPI, the demand for high-grade NPI by stainless steel mills first decreased and then increased in Q1. Stainless steel production continued to grow positively. Due to the strong cost support from rising raw material prices, stainless steel mills adjusted their production product models to expand profits, leading to a decrease in the proportion of high-nickel varieties and a decline in weighted nickel consumption MoM. However, overall monthly demand remained above 110,000 mt Ni. Overall, in Q1, China’s cumulative demand for high-grade NPI was 355,500 mt Ni, up 12.8% YoY. In Q2, the demand for high-grade NPI first increased and then decreased. After experiencing a sharp decline in 304 prices, the marginal profits of stainless steel mills were impaired. Mainstream stainless steel mills produced high-nickel and some special steel varieties to hedge against finished product price risks. The expansion in the proportion of high-nickel varieties drove up weighted nickel consumption. Although stainless steel production remained stable in May, the demand for high-grade NPI showed a steady increase. Overall, in H1 2025, China’s cumulative demand for high-grade NPI was 720,100 mt Ni, up 9.98% YoY.

IV. Market Outlook for High-Grade NPI in the Second Half of 2025 (2025H2)

Supply side, Indonesia still has plans for new capacity additions in 2025H2. If these projects are commissioned as scheduled, Indonesia’s annual capacity for high-grade NPI will increase by 61,600 mt Ni. Additionally, from the ore perspective, Indonesia’s current RKAB quotas are more relaxed compared to 2024. Coupled with a significant increase in nickel ore shipments from the Philippines to Indonesia, it is expected that smelters’ nickel ore inventories will remain healthy, without posing constraints on overall production. It is anticipated that Indonesia’s high-grade NPI production in 2025H2 will maintain an increase compared to H1. Domestically, following the rise in Indonesian demand, nickel ore prices in the Philippines have surged, imposing a heavier production burden on domestic smelters. It is projected that in 2025H2, the production of high-grade NPI by domestic integrated stainless steel mills will continue to decline, while traditional smelters may experience limited growth during the “September-October peak season”. Overall, the supply side is expected to continue growing in 2025H2.

Demand side, on July 1, the Sixth Meeting of the Central Financial and Economic Affairs Commission discussed issues such as advancing the construction of a unified national market, with “regulating enterprises’ low-price and disorderly competition in accordance with laws and regulations, guiding enterprises to enhance product quality, and promoting the orderly exit of outdated capacity” as one of the six major work directions for advancing the construction of a unified national market. The domestic stainless steel market has received positive signals for “combating the rat race” competition. Additionally, with the marginal easing of bilateral tariffs between China and the United States, sentiment has turned more bullish both domestically and internationally. It is expected that domestic demand resilience will persist in 2025H2, with positive growth expectations for external demand. Stainless steel production is expected to maintain or increase, leading to a strong demand outlook for high-grade NPI.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market exchanges, and relying on SMM’s internal database model, for reference only and do not constitute decision-making recommendations.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.