Our Terms & Conditions | Our Privacy Policy

Mint Explainer | What India Inc’s Q1 results mean for market investors

Mint takes a look at the winners and losers of the Q1 results season, and key takeaways for investors.

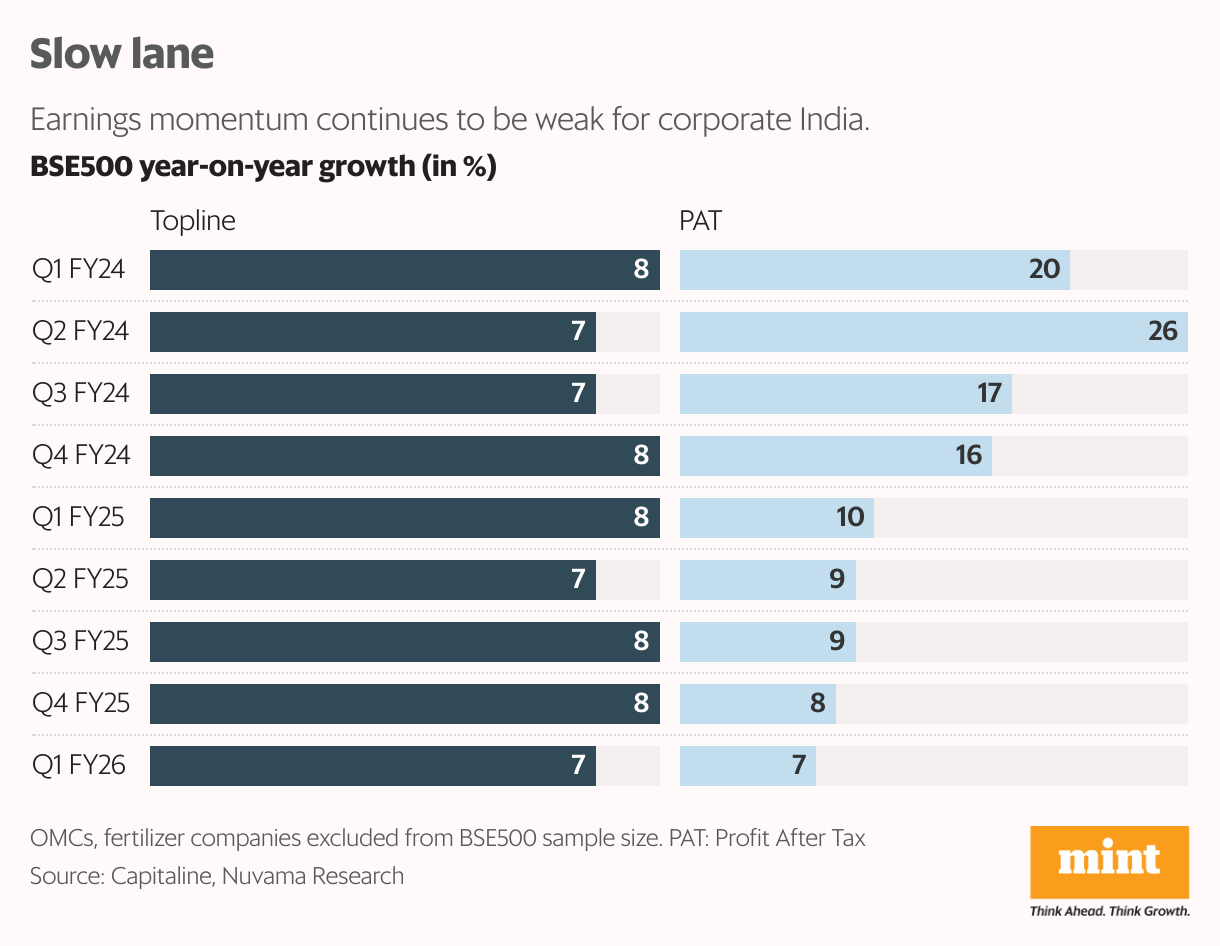

How did India Inc perform in the first quarter of FY26?

It has been a subdued start to the financial year. BSE500 companies (excluding oil marketing companies) posted a topline and profit growth of 7% YoY. This trend of single-digit growth was prevalent in FY25 as well. “BSE500 profits have now reconciled with the weak top line. The moderation in profits is now seen across the board,” Nuvama Institutional Equities noted.

Profit growth of small and mid-caps decelerated after an uptick in the preceding quarter. Frontline companies fared marginally better. The Nifty50 delivered net profit growth of 8% on-year compared to 3% in the preceding quarter. However, analysts at Motilal Oswal pointed out that Nifty reported single-digit earnings growth for the fifth consecutive quarter since the pandemic (Jun 2020).

“Five Nifty companies—Bharti Airtel, Reliance Industries, SBI, HDFC Bank, and ICICI Bank— contributed 77% of the incremental YoY accretion in earnings. Conversely, Coal India, Tata Motors, IndusInd Bank, ONGC, HCL Technologies, Kotak Mahindra Bank, Axis Bank, Eternal, HUL, and Nestle contributed adversely to the earnings,” they added.

Interestingly, several companies reported higher-than-expected other income, which increased 31% YoY for Nifty50 companies in Q1.

How did the banking sector fare during this quarter?

Banks witnessed further weakness in credit growth, moderation in net interest margins (NIMs) and asset quality stress in a few segments such as microfinance.

Credit growth was impacted by Q1 seasonality, continued caution in the unsecured segment and steady moderation in retail credit growth (+12% yoy), while credit to industry also remained subdued.

“We note that housing credit and vehicle credit growth have softened further at 10% yoy and 6% yoy, while unsecured credit growth, such as credit cards, has moderated from 30% yoy in 1QFY25 to 7% yoy in 1QFY26,” Kotak Institutional Equities said.

Most industrial sectors continue to witness muted credit demand, while bank credit to NBFCs moderated further in 1QFY26 to 3% YoY.

Real estate loans (+15% yoy) and trade loans (+11% yoy) are among the few pockets that are seeing strong bank lending in the non-retail segments.

That said, most banks reported decent deposit growth, with private banks outpacing their public sector peers. However, banks saw lacklustre growth in low-cost CASA deposits, which added to their margin headwinds.

“NIM compression was imminent during the quarter, with repo rate actions reflecting on yields. However, larger private banks (ex-Kotak) and PSU banks fared better than expected and managed margins better, reporting a shallow NIM contraction (7-12 bps). On the other hand, most mid-sized banks (18-30 bps) and SFBs (40-60 bps) in particular reported sharp margin contraction, further aggravated by higher interest reversals,” Axis Securities noted.

What trends were visible in the consumption space?

FMCG players had a decent showing, with both revenue and volumes recording healthy gains. Green shoots in urban consumption are evident, driven by higher discretionary income following RBI’s rate cuts, Budget’s income tax relief and slowing retail inflation, which is at an eight-year low.

Rural growth maintained its steady momentum. However, the early onset of monsoon impacted demand in categories like aerated drinks, juices and sun/skin care products. Robust demand was seen in biscuits, noodles, kitchen foods, edible oil, tea and coffee.

Companies are also hopeful of a steady raw material environment through FY26, setting the stage for margin improvement from the second quarter. However, Ebitda performance in Q1 was constrained by elevated raw material inventory costs and price fluctuations.

However, it was a summer to forget for consumer durables categories like air conditioners and coolers, which suffered a 30% YoY decline due to the early onset of the monsoon. Fans and refrigerators, too, witnessed contraction. The wires and cables segment saw double-digit volume growth, led by high infra demand and up-stocking by trade amid rising copper prices.

Premiumisation has been a rising trend across categories, which also drove margins. For automobiles, while revenue growth was supported by robust demand for SUVs and higher-priced offerings, overall Ebitda performance was muted owing to subdued volumes and cost pressures.

What did the IT sector’s report card look like?

In one word, underwhelming. Four of the five largest IT companies posted a sequential decline in revenues on a constant currency basis. Even mid-tier firms, which have outperformed their larger peers in recent times, are beginning to see signs of strain, with revenue growth slowing in Q1 FY26 compared to the past few quarters.

The top three players also reported a year-on-year contraction in Ebit margins, reflecting broad-based pressures on profitability. Over the past few years, companies had managed to safeguard margins during demand slowdowns by leaning on cost rationalisation, operational efficiencies, and wage adjustments.

However, after nearly three years of muted growth, these levers have been largely exhausted, analysts at Kotak noted.

Adding to this is GenAI, which is upending traditional staffing models and shaking the foundations of IT services pricing.

“With 35-45% of industry revenues tied to ADM (application development and maintenance services), even partial automation poses a meaningful headwind. We estimated that up to 10-15% of current revenues could come under pressure as clients start getting more for less, making productivity a structural challenge,” Motilal Oswal said.

“Indian IT sector’s legacy business deflation is nothing new: what is biting is the absence of a new technology cycle to replace the old. During earlier transitions (e.g., from IMS to cloud, or from legacy app development to digital), vendors were quick to scale up new offerings that more than compensated for the decline in older lines of business,” it added.

How did other major sectors perform in Q1?

Capital goods companies reported some moderation in their domestic revenues, but power electrical equipment players continued to enjoy robust execution, all-time high order books and multi-year high operating margin levels driven by better pricing power and favourable product mix.

“Order inflow growth for the capital goods sector was better than our expectations. It was particularly buoyed by the continued momentum in power T&D and renewable space. Overall, EPC companies’ inflows jumped 28% YoY, with L&T and KPIL witnessing strong double-digit YoY growth on the back of domestic and global wins. However, KEC experienced a temporary slowdown due to timing and bidding discipline,” Motilal Oswal said.

Cement companies witnessed high single-digit volume growth on the back of improved government spending on road and highway projects, while price hikes aided realisations. However, power and fuel costs showed an uptick in the quarter.

Larger pharmaceutical companies clocked a decent showing, even as exports saw weak growth. Companies are anxiously watching US policy changes regarding tariffs.

OMCs reported strong Ebitda and PAT growth as marketing margins surged because retail prices were unchanged despite a drop in global crude oil rates. However, city gas distribution (CGD) logged weak earnings due to a reduction in gas allocation and stronger LNG prices, which hurt their margins.

Real estate players saw continued momentum in residential demand on both volume and value basis. Strong growth in pre-sales was driven by companies like DLF, Prestige and Sobha which are expanding their footprint away from their home markets.

“However, we note that the six major metro cities have seen a moderation in new launches in the past few months, while sales volumes have weakened in aggregate. As a result, inventory levels have increased in recent months,” analysts at Kotak added.

The electronics manufacturing services sector too reported another stellar quarter, with aggregate revenue surging 66%, driven by the execution of a strong order book.

What do the Q1 numbers mean for investors?

Overall, the Q1 results season has been a sobering reminder that corporate India faces more headwinds than tailwinds at this juncture. BSE500’s top-line growth has remained in single digits for the ninth consecutive quarter. Revenue growth for even core companies (ex-commodities and BFSI) remained subdued in Q1FY26.

The post-covid profit recovery was largely led by margin expansion on the back of lower interest expense and better pricing power. However, with margins for many sectors close to decadal highs, the near-term outlook for profitability looks clouded.

“Consensus is, however, forecasting further margin expansion for most sectors—we think this could be difficult to achieve, unless demand improves or there is a supply-side tailwind from oil prices,” Nuvama noted.

Small and mid-cap companies, too, are facing challenges on the margin front, and can see more downsides than their large-cap peers.

“For FY26, consensus is forecasting a significant bounce in SMIDs’ profitability compared with large-caps. We think they could disappoint as growth is slowing down in a broad-based manner with even some domestic indicators—credit growth, auto sales and RE sales—slowing,” Nuvama added.

If small and mid-cap companies’ profits continue to disappoint compared to large-caps, this poses risks to their elevated valuation premiums, it added.

However, some analysts believe that the worst is behind, with the severity of earnings cuts moderating in Q1 compared to previous quarters, even as the trend of a higher number of downgrades continued into this quarter.

“EPS growth for Nifty-50 is projected to rise to ~9% in FY26 (vs. an anaemic 1% in FY25) – aided by a likely improvement in the macro environment owing to the stimulative fiscal and monetary measures. While the Indian equity market has been volatile over the past two months owing to tariff jitters, we believe that improved earnings prospects and reasonable valuations (barring small-caps) should enable the market to achieve modest gains,” Motilal Oswal said.

India Inc is also likely to get a boost this festive season, with Prime Minister Narendra Modi announcing a major revamp of the goods and services tax (GST) in his Independence Day speech.

The government is working on scrapping the 12% and 28% GST slabs, among other reforms.

“Rationalisation of GST rates should boost discretionary consumption by meaningfully lowering prices for end consumers. Importantly, reductions in GST rates could help reduce the burden on low-income households the most, given indirect tax structures are regressive in nature,” analysts at Morgan Stanley said, noting that the share of indirect taxes in total gross taxes has declined from 44.8% in F2015 to 41.5% in F2025.

“Moreover, an improving trend in aggregate demand is likely to improve business sentiment, supporting higher capacity utilisation rates, which would ultimately augur well for the labour market outlook and private capex activity,” they added.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.