Our Terms & Conditions | Our Privacy Policy

Ceat Ltd has completed the acquisition of Michelin Group’s Camso Construction Compact Line Business, effective 1 September. The integration is expected to take four to six quarters, the management said during an analysts’ call on Friday.

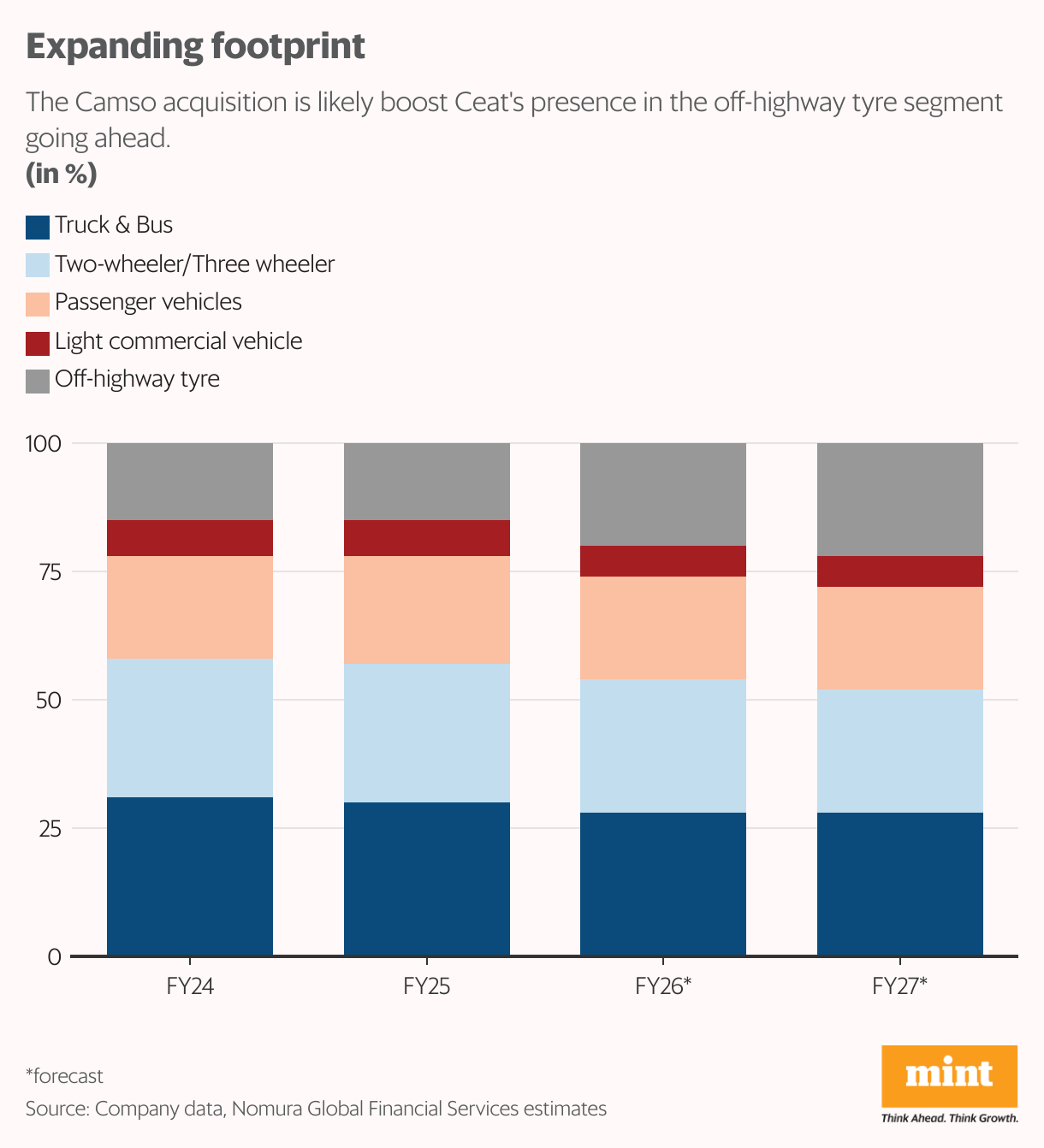

The deal, announced in December, is in line with Ceat’s strategy of driving growth through premiumization, globalization and a stronger presence in the off-highway tyres (OHT) segment. Camso has an installed capacity of 250 tonnes/day, evenly split between tyres and rubber tracks, though current utilisation is about 50%.

While the benefits of the acquisition will accrue gradually, the transition brings near-term risks. The global OHT and mining segment is facing challenges. Camso’s revenue fell to $150 million in 2024 from $215 million in 2023. Ceat’s management expects Camso to clock $130-150 million this year. The initial revenue and margin recognition would be lower as sales will be routed through the Michelin network.

Ceat will also procure semi-finished material from Michelin until it sets up its own upstream equipment. Once integration stabilizes, management expects Camso to deliver an Ebitda margin of around 20% by FY28. For now, the deal is expected to be earnings per share (EPS) dilutive. JM Financial Institutional Securities has cut its revenue estimates by 3.9% and 3.6%, translating into EPS declines of 12% and 8% for FY26 and FY27, respectively, due to delayed revenue and margin recognition.

On the balance sheet, Ceat’s net debt will rise. The company plans to invest $30 million in Camso over the next two years. Of the $225 million acquisition cost, $138 million has been paid, $43 million is due in FY27, and the balance in FY29, the management said. Nuvama Research estimates net debt to increase from ₹1,900 crore in FY25 to ₹2,900 crore in FY26 following the Camso takeover, before moderating to ₹2,400 crore by FY28 aided by positive free cash flows.

In the India business, management expects the recent GST rate cuts on two-wheelers, passenger vehicles, truck tyres and tractor tyres to support affordability. Domestic natural rubber prices have eased from ₹200–205/kg a month ago to ₹191–192/kg, but Ceat does not expect a significant margin benefit due to a marginal rise in global rubber prices and rupee depreciation. Consolidated capex for FY26 is projected at ₹1,000 crore.

Ceat’s stock trades at FY27 price-to-earnings multiple of 14x, as per Bloomberg data. While valuations appear reasonable, near-term triggers will depend on demand trends in the replacement segment and movements in input costs.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.