Our Terms & Conditions | Our Privacy Policy

The IPO arrives at a pivotal time for the solar industry, as governments worldwide push to reduce carbon footprint and shift toward renewable energy sources. The Indian government’s ambitious renewable energy targets have created a favourable environment for companies like Waaree Energies.

With a focus on solar power, the company has been instrumental in driving the transition towards cleaner and more sustainable energy sources. Besides, with an installed capacity of 12 gigawatts (GW), it stands out as a leading player in the country.

Strong financials

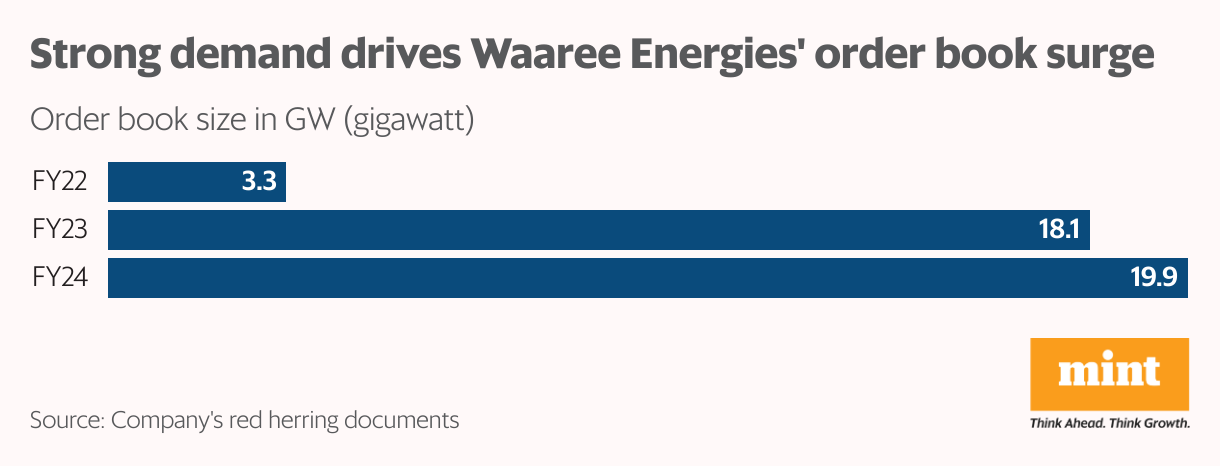

Waaree Energies has shown strong financial performance, with its order book surging sixfold to 19.9 gigawatts (GW) in the last three years. In the process of enhancing its backward integration capabilities, it aims to utilize the proceeds to set up an integrated 6GW ingot, wafer, cells and modules factory. “This backward integration allows the company to manufacture essential solar components, enhancing operational control and margin expansion,” said Shiwani Kumari, senior analyst at Monarch Networth Capital. “As capacity increases, operational leverage will come into play, providing the company with significant scale benefits.”

The company’s export-focused strategy has paid off, resulting in strong operating margins. Moreover, with revenues nearly quadrupling to ₹11,633 crore in 2023-24 and return on capital employed at an impressive three-year median of 26%, Waaree stands out in India’s solar energy sector.

Waaree Energies has also demonstrated remarkable financial discipline, achieving profitable expansion without relying on debt. This lean approach positions the company favourably compared to its peers, who often carry heavier debt burdens.

The company’s debt-to-equity ratio stood at an impressive 0.08 times in 2023-24, far below competitors like Websol Energy System and Premier Energies.

Amit Paithankar, chief executive of Waaree Energies, told Mint: “While we may need to draw down some debt for large capital projects, we will remain extremely cautious about how much we take on.”

Ajay Garg, director and CEO at SMC Global Securities Ltd, said that by managing debt carefully and leveraging economies of scale, Waaree can preserve its financial advantage. “However, the risks associated with increased leverage must be weighed against the potential rewards of enhanced capacity and market share.”

Echoing similar thoughts, Sonam Srivastava, founder and fund manager at Wright Research, noted that while aggressive growth can lead to increased revenue and market share, it also carries the risk of higher debt levels and potential operational challenges. “To mitigate these risks, Waaree Energies should carefully balance its expansion plans with prudent financial management,” she added.

Client concentration

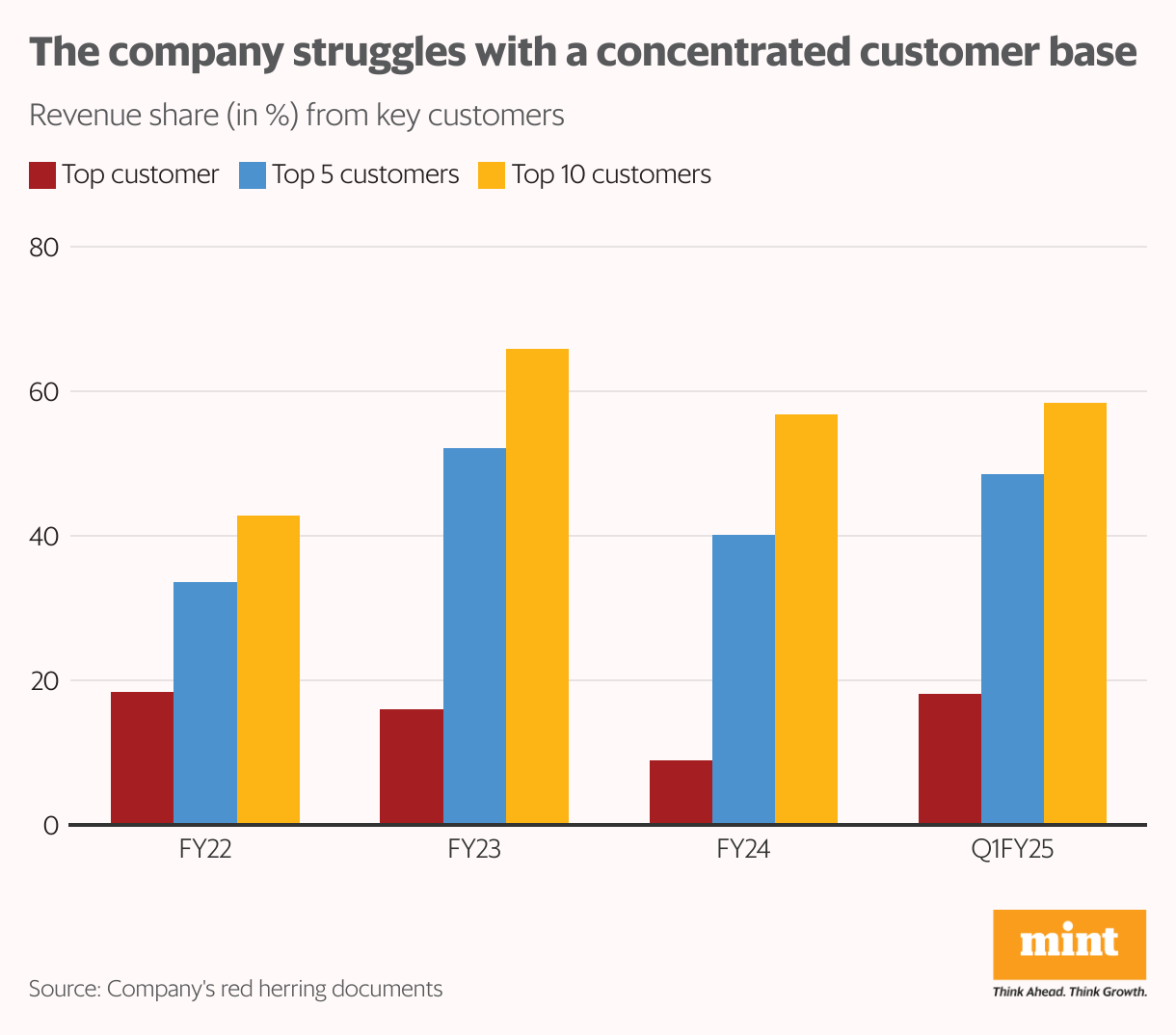

While Waaree has carved out a unique path, it faces risks tied to customer concentration. In the last fiscal, almost 57% of its revenue came from the top ten customers, while the top five had a 40% share. “Customers are sticky—they want to be with us once they work with us,” said Paithankar, highlighting the loyalty of key clients. However, he also acknowledged the need to diversify. “As we build capacity up to 21GW, we will explore other markets, particularly in Europe and beyond.”

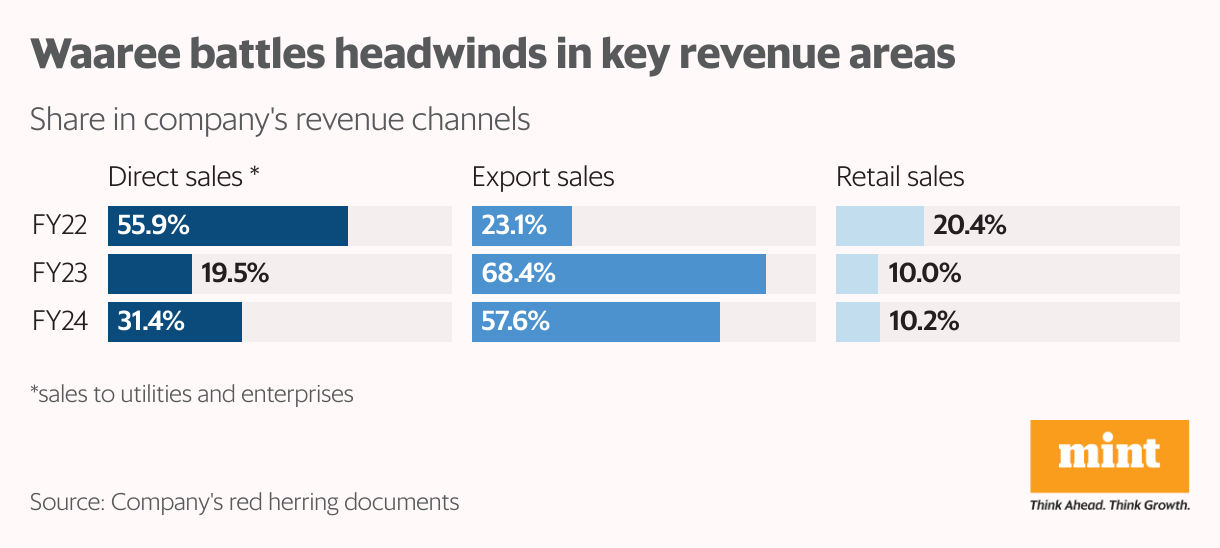

Furthermore, Waaree’s revenue share from direct sales, one of its key revenue channels, has seen a notable decline, plummeting from 56% in 2021-22 to 31.4% in 2023-24. Paithankar attributed this fluctuation to the inherent variability of the market, noting that sales can experience significant month-to-month and quarter-to-quarter swings. “Sometimes, we will have a high contribution from exports, which fluctuates based on customer requirements. Our rolling plan adapts to these changes, with annual plans divided into quarters and months.”

Meanwhile, Kumari noted that fluctuations in direct sales to utilities could result from various factors, including the timing and scale of large projects, which can vary annually. She observed that Waaree capitalized on the US ban on Chinese modules, leading to a surge in export sales, which increased from 23% in 2021-22 to 68.4% in 2022-23. “Waaree is building a more diversified customer portfolio and expanding its reach across enterprises and the retail segment, reducing dependence on any single market. The company is well-positioned to capitalize on the global energy transition and aims for a balanced split between domestic and export market sales,” she concluded.

Sino-American dependence risks

Moreover, its supply chain is highly exposed to disruptions due to its heavy reliance on Chinese imports, accounting for more than 80% of its total procurement during April-June 2024 period. Kumari admitted that the company faces several risks due to its dependency on imported raw materials from China, including supply-chain disruption, price volatility, and geopolitical risk. “China’s dominance over 75% of solar module production exacerbates these risks.”

To mitigate such risks, experts stressed the need for diversification. “Waaree’s reliance on Chinese imports exposes it to geopolitical and supply chain risks. Sourcing from multiple countries can enhance resilience,” Srivastava added.

The company’s shift towards backward integration seems to be a step in the right direction, as imported materials accounted for around 90% of total purchases, and duties imposed by the Indian government have impacted costs.

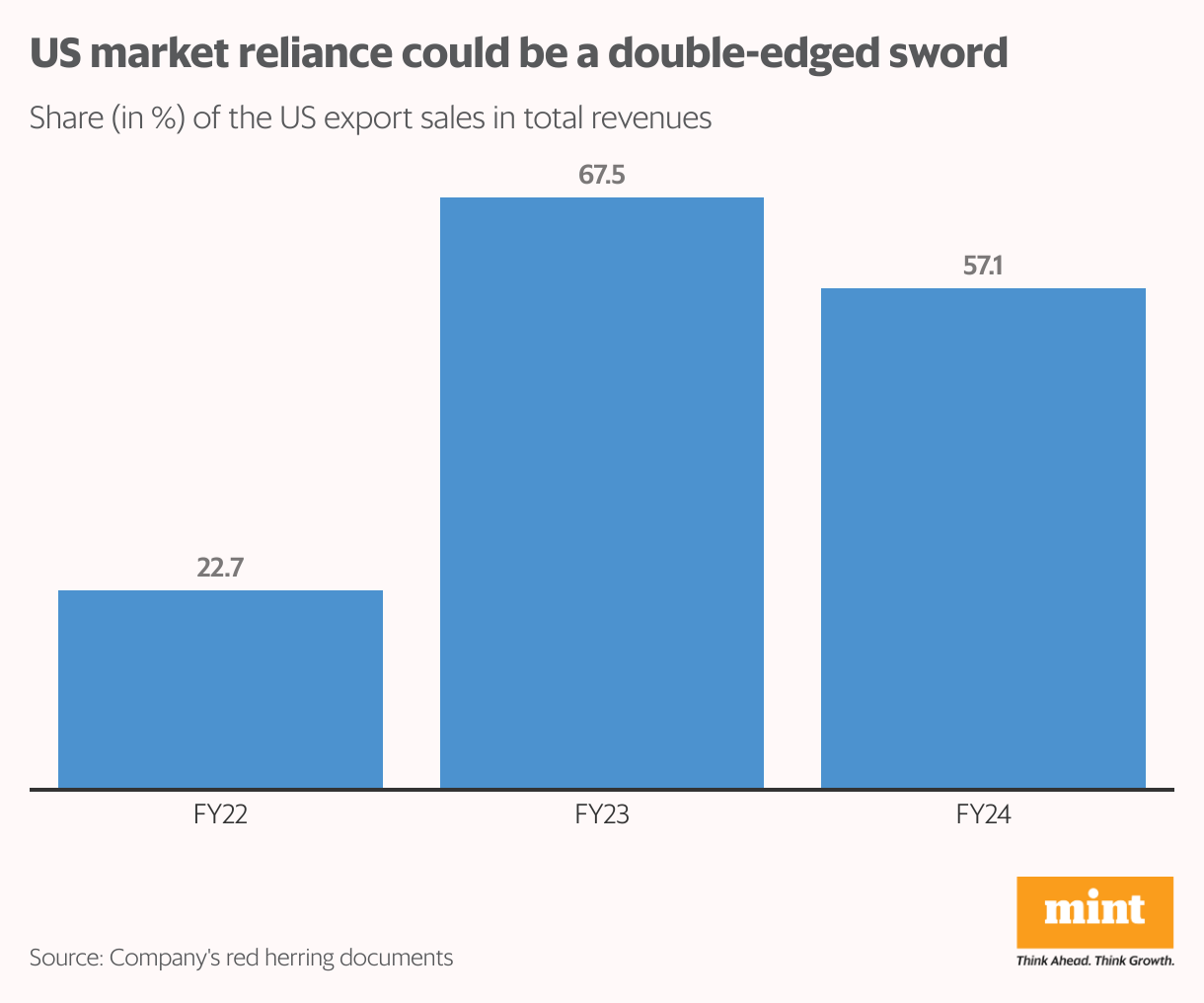

Additionally, Waaree’s export revenue is heavily concentrated in the US market, accounting for 57% of its total exports in 2023-24, exposing the company to potential risks associated with fluctuations in the US economy or changes in trade policies. “Waaree’s dependence on the US market and the lack of long-term contracts could impact revenues during a recession, but the 16.6GW order book offers some protection,” noted Vishnu Kant Upadhyay, assistant vice president-research and advisory at Master Capital Services.

However, Garg expects the company to remain resilient amid a potential US recession, given the global green energy shift, though competition from domestic US manufacturers could pose challenges.

Moreover, the risks of a looming US economic slowdown cannot be ignored. “A US recession could reduce solar product demand and complicate matters with currency fluctuations or trade barriers,” Srivastava noted. “Waaree should diversify its export markets, boost domestic sales, and explore new product lines to ensure long-term resilience,” she added.

Sun-powered profits

India’s renewable energy capacity is poised to nearly double between 2022 and 2027, with solar PV technology driving three-quarters of this expansion. Both India and the US are poised for solar energy dominance, with projected growth of 2.5 times by 2028. India’s solar PV capacity is expected to rise from 73GW in 2023 to 181GW by 2028, while the US is forecasted to grow from 138GW to 298GW over the same period.

“Waaree is well-positioned to lead and capitalize on the global energy transition. The company ultimately aims to achieve a balanced split between domestic and export market sales,” said Kumari.

As Waaree embarks on this new chapter, investors will be closely watching to see if the company can successfully navigate the challenges and capitalize on the opportunities presented by the burgeoning solar energy market.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.