Our Terms & Conditions | Our Privacy Policy

But let’s begin by understanding Raymond Lifestyle’s various business segments and its competitors in each of those.

Branded textiles

Raymond is well-known for its worsted suiting fabrics, including poly-wool, all-wool, silk, and other blended fabrics used in making garments such as suits and its shirting fabrics, such as cotton and linen. The company has about a 65% market share in the worsted suiting segment. Competitors in this consumer-facing space include Arvind Ltd and Vardhman Ltd.

Branded textiles are Raymond’s highest revenue contributor, accounting for about 50% of its topline in 2023-24. The company’s branded textile unit reported revenue of ₹3,449 crore for FY24, with an Ebitda margin of 20.5%. The segment is clearly a cash cow for the company.

Branded apparel

Raymond sells apparel under four brands to consumers. Its Raymond Ready to Wear and Park Avenue brands offer formal apparel. ColorPlus offers trendy casual and formal apparel, and Parx sells casual clothing for young people.

The Raymond Shop, which was started in 1958, has more than 1,100 stores across 380 towns and cities in India, selling these four brands.

The company’s Ethnix by Raymond brand includes ethnic wear such as sherwanis, kurtas, and jackets, which are sold in 114 stores. According to chairman Gautam Singhania, Raymond plans to add at least 100 Ethnix by Raymond stores in FY25.

The company also sells customized suits, jackets, and shirts to customers through its Raymond Made-to-Measure business.

Raymond’s branded apparel business is its second-largest segment. In FY24, it contributed about 23% of the company’s total revenue, with an Ebitda margin of about 11.5%.

Its main competitors in this segment are Arvind, Aditya Birla Fashions and Retail Ltd, Tata Group’s Trent Ltd, and Shoppers Stop Ltd for ready-made apparel; and Vedant Fashions for ethnic wear. However, these competitors also offer women’s wear.

Garmenting

Raymond’s garmenting business supplies ready-made clothes to multinational brands through its subsidiaries—Silver Spark Apparel Ltd for suits, EverBlue Apparel Ltd for jeanswear, and Celebrations Apparel Ltd for shirts. Competitors in this segment include Arvind Ltd, Gokaldas Exports Ltd, and KPR Mill Ltd.

The garmenting business contributed nearly 15% of Raymond’s total revenue in FY24, with an Ebitda margin of 10.3%.

High-value cotton shirting

Raymond Group sells high-quality cotton and linen fabrics to both domestic and international brands. This segment contributed about 12% of its total revenue in FY24, at an Ebitda margin of 11.4%.

Raymond Home

The group launched Raymond Home in 2013 to sell home textile products such as aprons, bedsheets, blankets, bathrobes, comforters, and table linen. Competitors in this space include Welspun Living Ltd and Trident Ltd.

Projections

Raymond Group’s decision to demerge into three listed entities—Raymond Ltd, Raymond Lifestyle Ltd, and Raymond Realty Ltd—and its growth projections reflect its desire to increase market share.

From about a 65% share in worsted suiting fabrics and a 5% share in ethnic men’s wear, the company is committed to increasing its reach by adding more than 650 retail stores over the next 3 years, with over 100 stores specifically for Ethnix by Raymond in FY25. The expansion will be mainly in Tier 1 and 2 cities and selectively in Tier 3 and 4 markets.

The company expects steady revenue growth of 12-15% over the next few years. This, in turn, is expected to double its Ebitda by 2028, per its growth guidance provided at its investor conference on 17 September. The company expects to lower its net working capital days to 60 from the current 76 and generate annual free cash of ₹600-700 crore.

Key financials

Raymond Lifestyle reported net revenue of ₹6,691 crore for the year ended March, adjusted for intersegment elimination and other income of ₹210 crore. With a gross margin of 46%, an Ebitda margin of 16.3%, and a profit-after-tax margin of 7.0%, it reported 97 inventory days and a net cash surplus of ₹227 crore as of 31 March.

The company’s operational return on capital employed was 31.7%, and operational return on equity was 10.4%.

As of September, promoters held about 54.7% of the company’s shares. Foreign institutional investors held about 12.6% of the shares, domestic institutional investors about 7.9%, and the public about 24.8%.

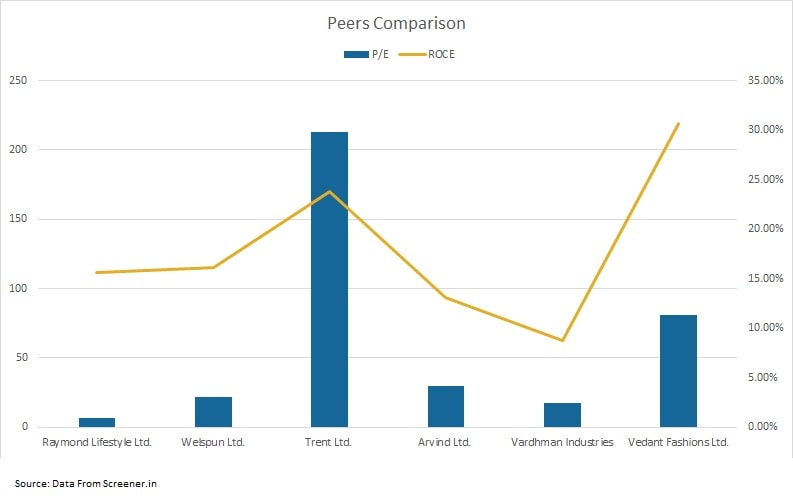

Comparison with peers

Multiple business segments, specifically those focused on men’s wear, make Raymond Lifestyle a unique company. Let’s now consider its key competitors across segments.

View Full Image

.

Raymond Lifestyle has the lowest price-to-earnings (P/E) ratio among its peers, and a better return on capital employed ratio, which shows the company’s profitability and capital efficiency.

Now getting to the question of whether Raymond Lifestyle can trigger a 37% rally. For this, the company is expanding its network of stores and counters as well as its product range, and expects to double its Ebitda by 2028. This is a positive sign for the company at large.

Also, adding ethnic wear, sleepwear and innerwear to its portfolio will increase its revenue and margin in the coming years.

In October, Motilal Oswal Financial Services Ltd, in its initiating coverage report on Raymond Lifestyle, recommended a “buy” on the company’s shares, stating that it expected the company to deliver an 11% compound annual growth rate in revenue and 15% CAGR in profit after tax over FY24-27. It set a target share price of ₹3,200 based on 30x the company’s September 2026 P/E ratio. This implies a return of 37% from current levels.

Note: We have relied on data from www.Screener.in as well as company’s presentation throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Mohit Bhambhani is a seasoned financial professional with over 13 years of experience in the field of financial research and corporate advisory. He also has substantial experience in Indian stock markets. With an analytical approach, he studies the performance of companies deeply, bringing value to the readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.