Our Terms & Conditions | Our Privacy Policy

Delhi-NCR leads with 57% growth amid nationwide housing price rally in Q3 2024 – Money News

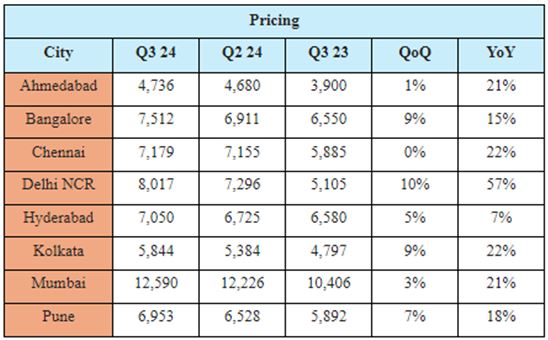

Property values in eight key residential markets across India have strengthened over the past year, driven by an increase in construction costs, according to data from PropTiger.com.

A recent report from PropTiger.com indicates that the average property prices in the majority of the cities examined saw double-digit increases in the third quarter of 2024 (Q3CY2024) when compared to the corresponding period in the previous year. The report, entitled ‘Real Insight Residential: July-September 2024,’ attributes this rise in prices to heightened demand, particularly for premium properties.

“The fact that the Reserve Bank has maintained a status quo on the repo rate at 6.5% in the past 10 policy meetings is adding further pressure on pricing. In the absence of a rate cut, developers as well as buyers continue to pay a comparatively high interest on loans, which ultimately impacts housing affordability,” the report said.

Also Read: Fixed Deposits vs Post Office Savings Schemes: Where should you invest for higher returns?

Delhi-NCR sees the highest annual jump in rates; Hyderabad the lowest

The report underlines a consistent annual growth in property prices for new supply and available inventory across the top eight cities. This sustained growth demonstrates the real estate sector’s resilience and adaptability in the face of evolving market conditions, it said.

According to the report, the highest annual jump in prices was seen in the Delhi-NCR property market, with a staggering 57% increase.

“The rising construction costs have necessitated adjustments to the basic selling price (BSP) of residential units in this market. The combination of strong end-user demand for luxury properties and renewed investor confidence have fueled the upward trajectory of housing prices here,” the report said.

The western cities of Ahmedabad and Mumbai, along with the southern tech hub of Bengaluru, all experienced healthy price appreciation in the 15-21% range whereas Chennai in south and Kolkata in east saw robust growth of 22% compared to the previous year, indicating strong economic activity and housing demand in these metros. This trend points to sustained demand in these economically vital centers.

Pune, often seen as a more affordable alternative to Mumbai, also saw an 18% increase, suggesting it’s maintaining its appeal for homebuyers while still seeing significant price growth.

Hyderabad, known for its IT sector, showed the most modest growth at 7%, indicating a more stable and mature market.

Quarter-over-quarter, most cities showed more modest increases or even slight plateaus. This could suggest that the market frenzy might be cooling off slightly.

Vikas Wadhawan, CFO, REA India & Business Head, PropTiger.com, said, “While we’ve observed significant price increases, especially in the prime localities of metro and mini metros, it’s crucial to view these developments through a wider lens of India’s economic growth trajectory and urbanisation patterns. The current market dynamics, characterised by a nuanced demand-supply equation, are creating a more stable and sustainable environment for long-term growth. This stability is particularly beneficial for end-users and serious investors. As we navigate through this phase, we anticipate a gradual alignment of buyer expectations with the new price realities.”

“Looking ahead, the real estate sector is poised to play a pivotal role in India’s economic narrative, driven by factors such as infrastructure development, smart city initiatives, and the growing prominence of tier-2 and tier-3 cities. The long-term outlook for Indian real estate remains robust, offering diverse opportunities across residential, commercial, and emerging asset classes for those who approach the market with a strategic, forward-looking perspective,” Wadhawan added.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.