Our Terms & Conditions | Our Privacy Policy

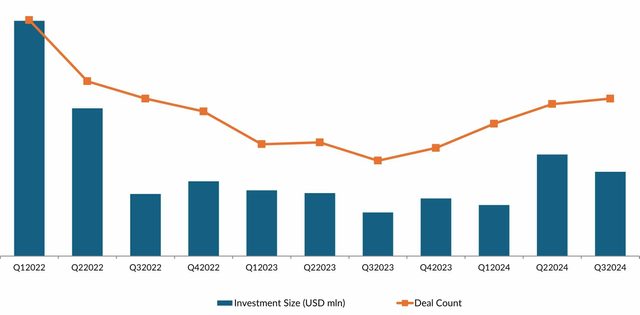

Indian startups secured $4.3 billion from private investors in the third quarter of 2024, marking a 17% decline after a sharp uptick in funding in the previous quarter, finds the latest report by DealStreetAsia – DATA VANTAGE.

Deal count increased marginally on a quarter-on-quarter basis to 343 transactions in Q3, according to India Deal Review: Q3 2024.

On a year-on-year basis, the total private funding garnered by Indian startups almost doubled in Q3 2024, while deal volume rose by 64%.

Funding secured by Indian startups

Source: DATA VANTAGE

In Q3, 11 mega deals – defined as those worth $100 million and more – raised a total of $1.96 billion, nearly 21% lower than the $2.47 billion bagged in the previous quarter. The top-funded startups during the third quarter include quick e-commerce startup Zepto, non-bank lender DMI Finance, mother and baby products retailer FirstCry, edtech platform Physics Wallah, and budget hotel chain startup OYO.

Three startups made it to the unicorn club in Q3 2024: MoneyView, Ather Energy, and Rapido.

Financial services tops fundraising tally

Financial services emerged as the most funded industry in Q3, with deal value up nearly 38% from the previous quarter. Digital lending company DMI Finance led the charts with a $334-million investment from Japan’s Mitsubishi UFG Financial Group.

Retail, which occupied the top spot in Q2, slipped to second place, with its quarterly proceeds dropping 48% from Q2 2024. The biggest retail transaction was closed by FirstCry, which raised $227 million from 71 anchor investors ahead of its initial public offering. Logistics/distribution reached third place, thanks to Zepto’s $340-million round.

Top industries by deal value in Q3 2024

E-commerce retained its top place among verticals in deal value, followed by fintech.

Growth-stage proceeds up marginally

Growth-stage funding — or investments at Series B and later — marginally rose in Q3 to account for about 53% of the total quarterly deal value.

Pre-seed and seed-stage deals drove deal count in Q3, but their proceeds tanked quarter over quarter. In contrast, pre-Series A and Series A deals recorded an increase in both deal value and volume during the third quarter.

According to the report, debt funding proceeds dropped to $457 million across 21 transactions in Q3 from $530 million across 32 deals in the previous quarter.

Bengaluru, Mumbai, and Gurugram were the top three destinations for venture investments in India in Q3, accounting for about 64% of the total investments.

Venture Catalysts, along with its accelerator fund 9Unicorns (now 100Unicorns), emerged as the top investor in Q3. During the quarter, it led investments in CricHeroes, NxtQube, Nautical Wings Aerospace, ReCircle, CoRover, and Sunfox Technologies, among others.

Pick-up in funding

Although the short-term outlook remains uncertain, private funding for local startups has improved in the last few months.

In the first nine months of 2024, the total funding raised by local startups increased 37% to $12.1 billion. Deal count, too, went up by 37% on a year-on-year basis to 966.

“There has been a recovery since the beginning of this year, and we hope the year ends on a positive note despite the not-so-good global and macro environment, which also speaks volumes about stability in the Indian market,” said venture capital firm Inflexor Ventures’s co-founder and partner Pratip Mazumdar.

The India Deal Review: Q3 2024 report offers data and insights on:

- Quarterly fundraising trends

- Top industries and verticals

- Top funding destinations

- Mega deal value and volume

- List of most active investors

Unlock the report for only $299 or upgrade to a Premium Plus subscription for greater savings and enjoy full access to up to 36 research reports a year, all for just $1200 ($100/month). Still not sure? Opt for a one-month trial.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.