Our Terms & Conditions | Our Privacy Policy

Two strong currents ran through this year’s IMF/World Bank Annual Meetings. First, many developing country governments are at high risk of debt distress. Second, economic growth prospects in developing countries have slowed to the lowest long-run rates in decades.

The themes are connected. According to IMF research, economic growth is the most powerful way to reduce the risk of debt distress. One eminent economist described the current situation as one with multiple equilibria, where developing countries have fallen into a bad equilibrium state in which countries are not growing, have a high risk of debt distress, can only attract capital at punitive interest rates, and hence have low growth. The solution: move to a good equilibrium state with high economic growth, reduced risk of debt distress, and lower interest rates that in turn support growth.

The question then becomes how to move from the bad to the good equilibrium.

In remarks delivered just before the meetings, U.S. Treasury Undersecretary Jay Shambaugh took the following position: “If you are a country committed to sustainable development and if you are willing to engage with the IMF and MDBs to unlock significant financing alongside significant reform measures, there needs to be a financing package from bilateral, multilateral, and private sector sources to bridge your liquidity needs in a way that is supportive of your sustainable long-run development.”

In a similar vein, shortly after the meetings, U.K. Chancellor Rachel Reeves delivered a budget that reflected her new thinking on what responsible fiscal policy looks like. She distinguished between tax-financed recurrent expenditures of the U.K. government and far higher levels of debt-financed public investments to spur growth.

Both these statements are a welcome departure from the orthodox position that the best approach to debt distress is fiscal austerity. This orthodoxy has been a straitjacket that leaves countries in the low-level equilibrium. With slow-moving processes to restructure or reprofile debt service payments, low-income (LICs) and lower-middle-income countries (LMICs) have sacrificed social spending and public investment. Their calls for more fiscal space—meaning access to finance that would allow for more government investment—moved to center stage during the Annual Meetings. The World Bank announced new financial policies that would permit it to increase lending volumes by an average of $15 billion per year over the next decade, while the IMF announced reduced fees and surcharges and a transfer of general resources that would more than double the pre-pandemic level of concessional support to LICs.

These official statements and policy measures reflect a recognition that a fiscally responsible government should invest whenever real social returns are higher than real interest rates.

Homi Kharas

These official statements and policy measures reflect a recognition that a fiscally responsible government should invest whenever real social returns are higher than real interest rates. In a previous post, I documented that almost all developing countries, despite their well-known policy and institutional shortcomings, still have investment opportunities that significantly outweigh the cost of borrowed money from official international financial institutions. For most of them, implementing such investments is the best way to improve creditworthiness and raise economic growth rates at the same time.

This is welcome news for developing countries who are currently confronting the following unpleasant facts. The average public spending on health was $9 per person and $34 per person annually in LICs and LMICs respectively in 2022. For education, it was $24 and $91 per person. WHO and UNESCO analysis suggests these figures fall woefully short of what is desirable for countries at these levels of development. While spending does not translate readily into outcomes in either health or education, it is difficult to imagine significant progress on human capital outcomes when public spending stays at these levels.

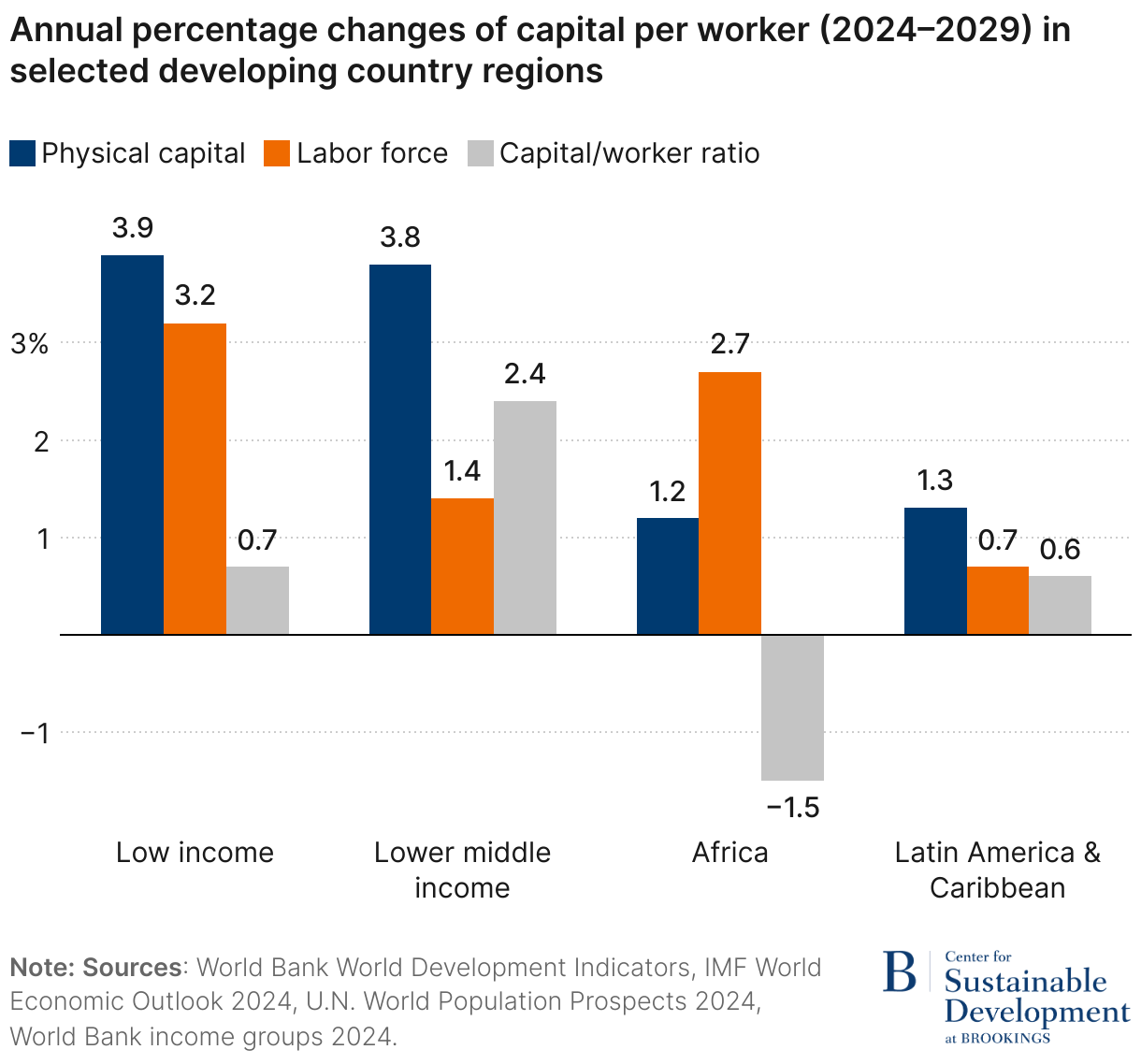

The same story of inadequate public spending for infrastructure, climate action, and nature holds in most developing countries outside East Asia and India. Figure 1 below shows the expected change in capital-to-labor ratios in developing country regions between 2024-2029, based on the IMF projections of gross investment rates for this period. Applying a commonly-used perpetual inventory approach, I calculated changes in capital-to-labor ratios, assuming a 5% depreciation rate and an initial-year average capital-to-output ratio of 4. These calculations draw on investment and labor force data in the World Bank’s World Development Indicators. The data is for total capital, rather than public capital, but previous research shows a very close correlation over time between public and private capital stock growth rates.

Figure 1

The data presented in Figure 1 suggest that, on average, there is a particular problem in low-income countries where labor force growth is high. There is also a problem in select middle-income countries. The figure shows that there is unlikely to be significant capital deepening under current trajectories over the medium term in Africa or Latin America. In Africa, the issue is particularly grave. Thanks to rapid growth in the working-age population of 2.5% per year, capital-to-labor ratios in Africa are likely to fall in the medium term. If this happens, low per capita growth becomes inevitable (Ezzahid and Rafik, 2024). Latin America is slightly better off—levels of investment are very low such that the capital stock is forecast to grow by only just over 1% per year, but because the growth of the labor force is also very low, there is some very modest capital deepening, albeit at only about 0.5% per year (ECLAC, 2023).

To give some sense of the likely impact of such low growth in capital stocks, Figure 2, reproduced from the IMF, shows that countries with low public capital growth rates also have low long-term GDP growth rates.

Figure 2. Countries with higher public capital growth rates also have higher real GDP growth rates

Source: IMF 2019, “Estimating the stock of public capital in 170 countries.”

Source: IMF 2019, “Estimating the stock of public capital in 170 countries.”

Taken together, this data shows how little scope there is for governments in these regions to transform their economies into sustainable and inclusive growth under current trajectories and orthodoxies. The chances for climate action, social improvements, conflict prevention, or delivery of any of the global or developmental goals that have been agreed to are slim if the current trajectory with its very low levels of investment and social spending are followed.

Relaxing the fiscal straitjacket by providing enhanced access to finance, including debt finance, from international financial institutions in cases where investment programs are sound and validated by these institutions is the welcome news coming out of the Annual Meetings. It seems to have support from IFI management, major shareholders, and developing countries themselves. Now, the debate shifts from strategy to tactics in specific country programs. As always, the devil is in the details, but the idea that developing countries should have an enhanced growth framework within which they can implement needed programs for climate action and invest in human capital is now more readily accepted by influential stakeholders of the international financial system.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.