Our Terms & Conditions | Our Privacy Policy

These factors have prompted many countries to invest in chip-making and design ecosystems, while diversifying supplies, the feeder networks for which are dominated by a handful of countries like the US, China, South Korea, Vietnam and Taiwan.

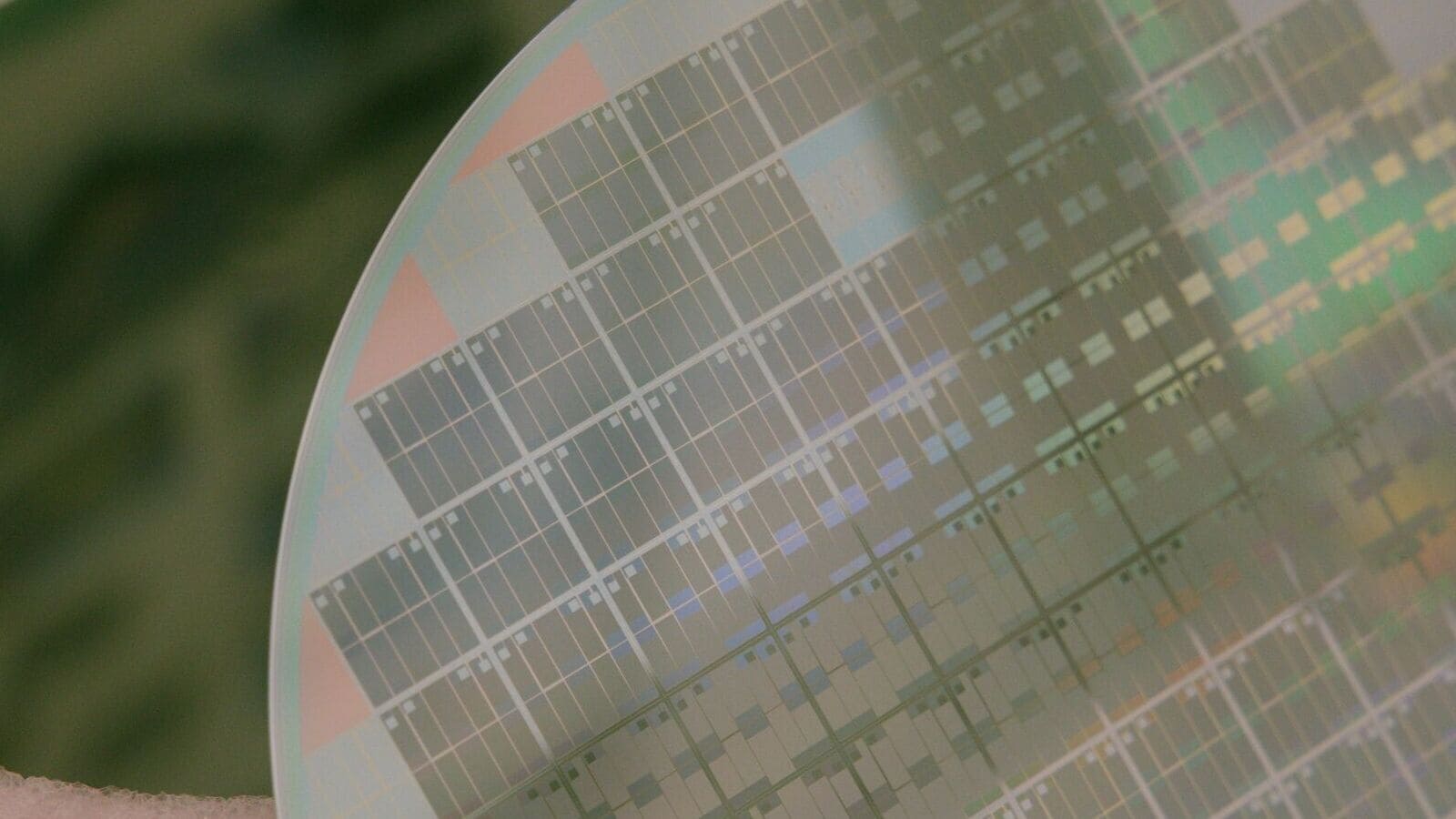

In setting up our own wafer fabrication units, or fabs, we expect to reduce costs as well as uncertainty over access to chips needed for electronic devices, drones, electric vehicles, solar panels and artificial intelligence (AI) applications. In the global context, this is clearly the way forth.

India’s US deal, signed last March, aims at semiconductor supply chain resilience, mutually beneficial research and development (R&D) and developing talent and skills. The EU agreement inked last November covers R&D and innovation, talent creation, partnerships and the exchange of market information.

The broader goal is to make India one of the world’s top five global destinations for chip-making by 2030. Joining hands with Singapore makes sense as it offers us better access to advanced technologies, a proficient workforce, cutting-edge tech universities, wafer-fab parks, a business-friendly environment, strong intellectual property (IP) protection and also a gateway to Southeast Asian markets.

The island state has attracted a vast roster of companies that design, manufacture, package and test chips, with many of the world’s major players among them. That said, while Taiwan makes high-end chips of 7 nanometre and less for smartphones, laptops and AI models, Singapore makes ‘mature node chips’—of 28nm or more, like fabs in India plan to—that are used in appliances, cars and industrial equipment.

Further, Singapore’s labour, fuel and electricity costs are the highest in Southeast Asia (nearly 15% more than in Malaysia, according to a BCG index). India, on its part, has a relatively inexpensive but strong talent pool in software engineering, industrial equipment and IC design, and is home to over 2,000 semiconductor design engineers.

Intel, Texas Instruments, Nvidia, AMD and Qualcomm have design and R&D centres here. Of course, we expect to host wafer fabs too. So far, New Delhi has approved four projects, worth over ₹1.5 trillion, including Micron’s and an alliance between Tata Electronics and Taiwan’s Powerchip Semiconductor Manufacturing Corp, all of which are expected to churn out 180,000 wafers a month once ready to roll.

With the Adani Group and Israel’s Tower Semiconductor also planning to set up a $10 billion semiconductor fab, we will have the building blocks for local microchip-making that cover the critical value chain of design, fabrication, assembly, testing, marking and packaging. India’s $10 billion fund meant to attract big chip-makers could move the needle further.

India, like Singapore, is not making high-end chips, but given that nodes of under 10nm account for less than 5% of global chip capacity, the strategy of making larger chips is sensible, as it takes lower upfront investments and these chips are unlikely to get outmoded too soon, a risk borne in the race at the AI-led front end.

Also read: India & Singapore Sign Agreements to Work on Semiconductors, Digital Tech | PM Modi in Singapore

With foreign deals and fabs, we may finally be able to ease our semiconductor struggles. But, even as we subsidize our chip goal by policy, we must ensure speedy execution of these projects.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.