Our Terms & Conditions | Our Privacy Policy

Automotive suppliers are under serious strain. Should new tariffs remain in place, North American car sales could decrease by a staggering 1.8 million units this year. Diminishing production volumes, lackluster consumer demand, and a slower-than- anticipated electric vehicle (EV) transition make it clear the industry is facing an unusually perilous moment.

Yet even these headwinds won’t stop the paradigm shift currently underway, one powered by unprecedented technological advancements, heightened competition, and a redoubled commitment to scale and sustainability. Mid- market suppliers that accelerate cost efficiencies, improve their speed to market, and invest in innovation will thrive in the months and years to come.

With consolidation likely to pick up, they’ll also be well positioned for potential merger and acquisition (M&A) opportunities. Here’s what dealmakers should know as they look to navigate the twists and turns ahead.

The Many Bends in the Road

2025 has both intensified existing challenges and engendered new obstacles for automotive suppliers, including:

Rising costs: Suppliers have to contend with elevated raw material and shipping costs, shortages of key supplies (including semiconductors), and higher wages due to skilled labor scarcity and recently concluded union contract negotiations.

Tariffs also could cause further cost spikes and disrupt existing supply chains. Even though trade agreements reached with the United Kingdom, European Union (EU), Japan, and South Korea ease some of the intense uncertainty surrounding automotive-related imports, trade agreements have yet to be reached with other key countries such as Mexico, Canada, Brazil, and India. Additionally, tariffs on key components like steel, aluminum, and semiconductors could increase costs for US-based manufacturers, which may lead to compressed margins and initiatives to conserve cash, including deferred investments.

At the same time, manufacturers must continue to invest in innovation and costly technological advancements to drive productivity, meet ever-stricter emissions and safety regulations, and adapt to vehicle connectivity technologies like vehicle-to-everything (V2X) and autonomous systems—adding new cost pressures for suppliers.

Heightened price sensitivity: With economic headwinds looming and prolonged elevated interest rates, consumers are prioritizing affordability over higher-priced newer features—holding on to their cars for longer, gravitating toward certified pre-owned vehicles, and embracing ridesharing platforms. In response, automakers are offering incentives like generous rebates and cheap financing to entice buyers, which in turn has pressured suppliers as original equipment manufacturers (OEMs) attempt to recoup margins by squeezing suppliers. However, as new- car affordability declines and vehicle lifespans increase, suppliers with exposure to the aftermarket segment are set to benefit from extended ownership cycles with sustained growth in aftermarket demand for maintenance and replacement parts.

Changing consumer preferences: Beyond affordability, the rise in urbanization with increased customer focus on flexibility and affordability is reshaping urban transportation. This is expected to reduce private vehicle ownership, leading to capacity realignment, sector-wide consolidation, and increased investments in subscription-based mobility-as-a-service (MaaS) and ridesharing platforms.

An uncertain green transition: Hybrids are gaining traction as a more practical alternative to fully electric vehicles, especially with government subsidies for EVs ending. The recently passed tax and spending bill will eliminate federal EV tax credits by September 30, so vendors with a focus on EV will need to diversify to stay afloat as demand stalls.

Intensifying global competition: China’s auto production doubles that of North America as ample technology investment, government incentives, and strong distribution networks have lowered manufacturing costs by 25 to 30 percent compared to their North American counterparts.

Tech mismatches: Investments in artificial intelligence (AI), the internet of things (IoT), autonomous robotics, and connected factories are helping suppliers streamline operations, reduce costs, and accelerate time to market.

However, investment in EV technologies has outpaced consumer demand—a mismatch that leaves OEMs and suppliers with surplus capacity and liquidity challenges, complicating future investments.

Consolidation Expected to Rev Up

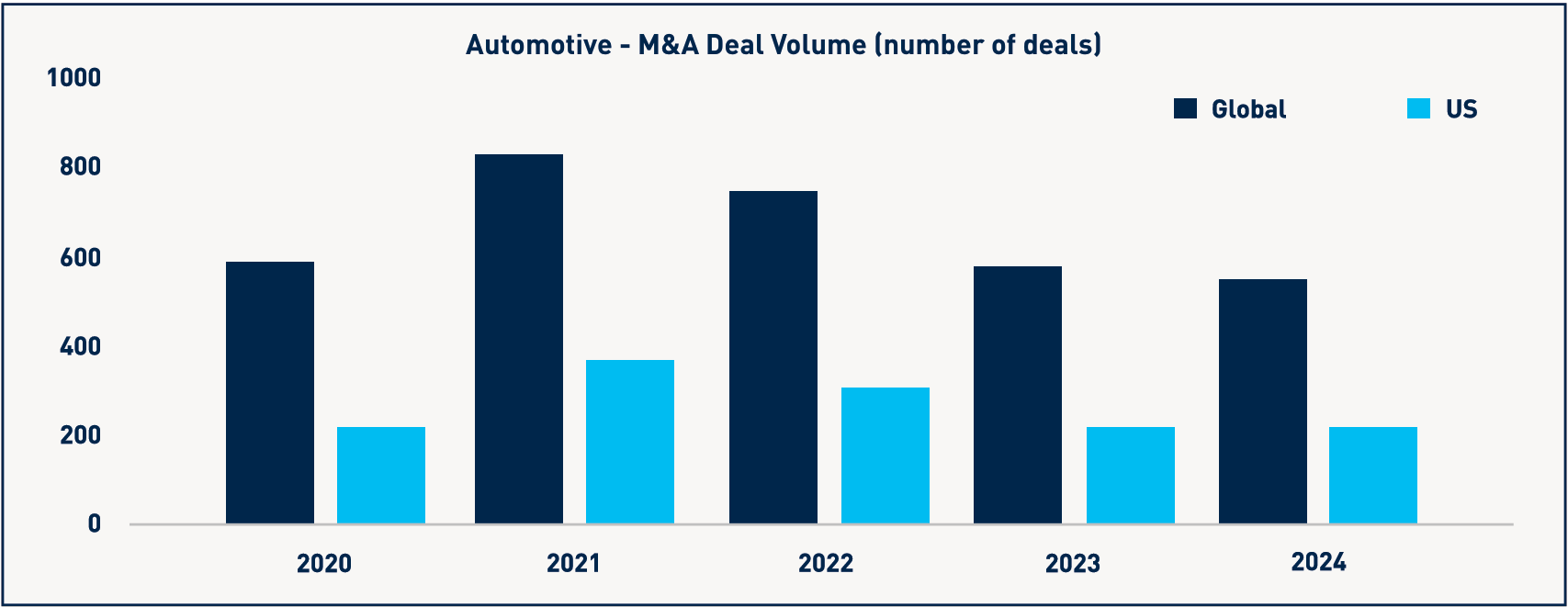

In light of these challenges, automotive suppliers are reassessing their relationships with OEMs, investing in leaner operations, rebalancing product offerings away from stagnating segments (e.g., from EV adoption toward next-generation components), and diversifying toward growth-oriented partnerships and aftermarket opportunities. Additionally, highly fragmented subsegments like repair and collision shops—alongside increased adoption of high-tech components, advanced driver assistance systems (ADAS), infotainment systems, and connectivity—could lead to promising M&A opportunities for middle-market suppliers over the next year in a welcome rebound from a relatively stagnant year for automotive M&A in 2024.

Source: S&P Capital IQ

Note: Represents announced deals and closed deals; excludes deals with EV below $50 million and above $1 billion.

Compressed profit margins and liquidity challenges could drive M&A too. OEMs are evaluating their manufacturing footprints and production portfolios, identifying strategic gaps and non-core divestitures that could lead to more deals. While some suppliers may exit the automotive industry entirely to manage liquidity, others are looking for scale through consolidation to better manage costs.

The broader reshoring movement—particularly amid mounting tariffs—is also likely to spur additional M&A activity, especially through partnerships and joint ventures that can help mitigate risk. And despite the slowdown in EV demand, interest in internal combustion engines (ICE) and hybrid vehicles remains strong, encouraging consolidation among ICE component suppliers.

More broadly, potential reductions in borrowing costs, increased political clarity in the US and EU, and the abundance of private equity capital are bolstering M&A optimism.

“The automotive industry is in a state of uncertainty and mounting cost pressures, and the answer for many companies will be to pursue partnerships and alliances instead of traditional M&A.”

D. Foucar et al., M&A in Automotive and Mobility: Hedging Bets until a Clear Future Emerges, Bain and Company (February 4, 2025).

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.