Our Terms & Conditions | Our Privacy Policy

India stands at an inflection point. What was once a regulatory checkbox is now a commercial opportunity. If we act decisively—backed by policy, state-level programmes, and platforms—we can unleash the largest untapped grid resource in the country: the demand side.

July 30, 2025. By News Bureau

Powering a Grid in Transition

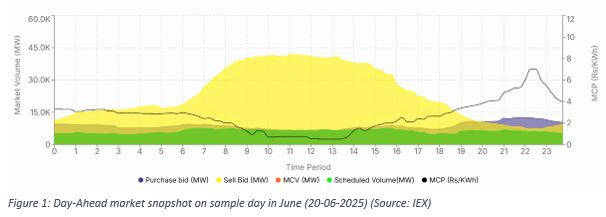

India stands at a critical juncture in its energy transition. With an ambitious goal to integrate 500 GW of non-fossil fuel capacity by 2030, the nation is confronting a monumental challenge to its grid stability. The traditional, predictable model of power generation following a steady consumer demand is being fundamentally disrupted by the intermittent nature of solar and wind energy. Power can be abundant on sunny, windy days, yet scarce on still, cloudy evenings, as evident in Figure 1, e.g., prices fluctuated from as low as INR 0.5/kWh during periods of abundant renewable generation to INR 7/kWh when supply tightened in the Day-Ahead market. Simply building more power plants is not a sustainable solution to this volatility.

How do we bridge this gap? The answer lies not in adding more supply, but in reshaping demand. It requires a paradigm shift: transforming India’s millions of electricity consumers from passive users into active, dynamic partners in balancing the grid. This isn’t just about Demand Response—it’s about unlocking Demand Flexibility: the ability to shape, shift, and optimise consumption in real-time, not just during emergencies.

According to the Central Electricity Authority’s (CEA) report on “Optimal Generation Capacity Mix for 2029-30”, India is expected to experience peak demand of ~335 GW by 2030. Demand-side pilots (short-term programmes by Indian DISCOMs to test user-side load adjustments) have demonstrated the potential to reduce peak demand by 1–3 percent. That translates to a national peak demand reduction of 3.4–10 GW, a significant contribution to grid stability and efficiency. As a service, Demand flexibility presents a sustainable pathway to a more stable, reliable and secure energy future.

Why demand flexibility is different – and essential

For years, the industry has focused on Demand Response (DR), which is the reactive process of consumers reducing their electricity usage in response to a direct signal, typically during a grid emergency or a high-price event. Think of it as an emergency brake for the grid. While DR tells a consumer to switch off appliances during a crisis, it is not a comprehensive solution for a modern grid.

Demand Flexibility (DF), in contrast, is the proactive, intelligent, and continuous evolution of this concept. It is the inherent capability of a customer to continuously and intelligently modify their electricity consumption in response to the grid’s real-time needs. It’s like a self-driving car constantly adjusting to traffic and terrain. It enables consumers to: Shift load to off-peak times (e.g., running chillers or pumps at night), Participate in ancillary services and help integrate renewables and avoid blackouts.

In an era of dynamic pricing and digital infrastructure, DF becomes a non-negotiable asset, not just for grid operators but also for consumers seeking cost savings and reliability.

Strengthening the Foundation: From Procedural DSM to a Profitable Grid Resource

In 2010, the Forum of Regulators (FoR) introduced Model Demand Side Management (DSM) Regulations that marked an important first step. While these regulations provided a procedural framework, early implementation focused primarily on load management, energy efficiency and basic demand response without a proper corresponding commercial incentive for utilities (DISCOMs). As a result, the broader opportunities of demand flexibility remained underexplored for several years.

Despite the initial intent for tailored adoption, around 30 states and UTs implemented these model regulations with limited customisation. Given the cost-plus tariff model, reducing electricity consumption often translated into reduced revenues for DISCOMs. This may have created unintended disincentives for more ambitious demand-side programmes. The immense potential of the demand side to act as a grid resource remained untapped.

The Turning Point: A Regulatory Revolution Towards Flexibility (Post-2022)

Since 2022, the tide has turned. Several landmark reforms have laid the groundwork for a national flexibility market.

- A National Market Gateway: The CERC (Ancillary Services) Regulations, 2022, were a watershed moment. They formally defined Demand Response as a resource for secondary and tertiary reserve ancillary services that could participate in national grid-balancing markets. This reframed flexible demand from “a saved megawatt into a dispatchable megawatt” resource, i.e. from electricity consumption reduction to a dispatchable reserve which could be compensated.

- A State-Level Blueprint for Action: While CERC opened the market, the Maharashtra (MERC) Demand Flexibility Regulations, 2024, provided a powerful state-level blueprint. Its mandatory Demand Flexibility Portfolio Obligation (DFPO) requires DISCOMs to procure a progressively increasing amount of flexibility each year, with direct financial incentives for exceeding targets and penalties for shortfalls. This masterstroke aligns the DISCOM’s financial interests with the goal of harnessing demand-side resources.

- Top-Down Policy Enablers: Supporting these regulations, the Ministry of Power’s push for mandatory Time-of-Day (ToD) tariff regime and Resource Adequacy (RA) guidelines has created the enabling consumer environment and planning discipline needed to make demand flexibility a core, cost-effective grid resource.

Global Best Practices: The Blueprint for a Flexibility Market

India does not need to reinvent the wheel. Global leaders offer proven models for building a market for flexibility, not just a programme for response.

- United States: Landmark orders from the Federal Energy Regulatory Commission (FERC), like Order 2222, have systematically opened wholesale electricity markets to aggregations of Distributed Energy Resources (DERs)—like rooftop solar, EVs, and smart appliances. The order also affirmed that the existing opt-out provisions for demand response programs do not apply to “heterogeneous” DER aggregations, which are groups of diverse assets that may include demand response alongside other resource types. It provided aggregators to compete on a level playing field with traditional generation.

- European Union: The EU’s “Clean Energy for all Europeans” package mandates that member states must allow and encourage demand-side participation through aggregation, ensuring third-party aggregators have non-discriminatory access to all electricity markets.

- Australia: The Australian Energy Market Operator (AEMO) implemented a Wholesale Demand Response Mechanism (WDRM), enabling DR providers to aggregate smaller loads and bid them directly into the national market, getting paid the wholesale spot price for their contribution.

Additionally, on the technology enablement side, international experience underscores the importance of open standards like OpenADR for enabling interoperability in DR systems. Robust cybersecurity measures, including end-to-end encryption, data anonymisation, regular security audits, clear consumer consent processes for data usage, and segregated networks for critical DR infrastructure, highlighted in FERC orders and EU Directives, are considered best practices. Key international standards series like ISA/IEC 62443 (for industrial automation and control systems cybersecurity) and IEEE 1547.3 (for cybersecurity of DERs) provide valuable frameworks.

These international examples highlight a common set of principles for a successful flexibility market: clear market access rules, value-based compensation, robust frameworks for third-party aggregators, and strong consumer protection.

The Road Ahead: A National Blueprint for Demand Flexibility

The recent progress is transformative, but to unlock the full potential of flexible demand, India needs a new, harmonised national model regulation. Building on the existing successes, the framework must create a robust and commercially viable ecosystem for all states and market participants. Key pillars of this national blueprint should include:

- Mandate a National DFPO: A national Demand Flexibility Portfolio Obligation, modelled on Maharashtra’s success, should be adopted for all DISCOMs to drive action.

- Standardise the Rulebook: A functioning market requires consistent rules for baseline calculation, cost-effectiveness tests, and, crucially, independent Evaluation, Measurement, and Verification (EM&V) to ensure performance is real and verifiable.

- Empower New Market Players: Much of India’s flexibility is in smaller homes and businesses. Aggregators—companies that bundle these loads—are key. The new regulation must grant them direct access to participate in all markets.

- Design for Commercial Viability: The framework must define clear payment streams, from dynamic pricing to “pay-for-performance” models, that offer both a capacity payment for being available and an energy payment to create predictable revenue for consumers and businesses.

- Future-Proof the Framework: Regulations must be agile to accommodate electric vehicles, battery storage, and smart homes, promoting open technology standards and ensuring cybersecurity and should thrive for a prosumer-driven landscape.

- Co-optimising Efficiency and Flexibility: A significant historical gap has been the failure to co-optimise Energy Efficiency (EE) and Demand Flexibility (DR). The new framework should encourage integrated programmes that pursue both permanent energy savings and temporary load modifications. This requires sophisticated M&V guidelines that can clearly distinguish between the two, ensuring each is valued and compensated appropriately.

- Spurring Innovation through Sandboxing: To accelerate the adoption of new technologies and business models, the framework should formally enable regulatory sandboxes. These controlled environments allow utilities, aggregators, and technology companies to test innovative approaches without being constrained by existing rules, paving the way for the next generation of grid solutions.

A Win-Win for the Entire Ecosystem

A robust demand flexibility market creates a virtuous cycle of benefits for all stakeholders:

- DISCOMs: Gain access to a cost-effective resource to manage peak demand, reduce procurement costs, and defer expensive network upgrades.

- Consumers: Benefit from lower electricity bills, enhanced grid reliability, and the potential to earn new revenue by participating in flexibility programs.

- Grid Operators: Achieve better grid balancing, reduce the curtailment of valuable renewable energy, and enhance overall system resilience.

- Technology Providers: Can capitalise on new business models in aggregation, automation, software platforms, and data analytics.

Activating the Grid’s Hidden Asset

India stands at an inflection point. What was once a regulatory checkbox is now a commercial opportunity. If we act decisively—backed by policy, state-level programmes, and platforms—we can unleash the largest untapped grid resource in the country: the demand side.

By aligning state mandates with national markets, and empowering every consumer—from factories to households—we can turn demand flexibility from a footnote into a frontline strategy for a reliable, clean, and affordable energy future.

Turning millions of consumers into active grid partners is no longer just an option; it is an economic and operational imperative. It is the key to ensuring a reliable, affordable, and sustainable energy future for all.

– Nitin Srivastava, Program Lead, Smart and Resilient Power and Mobility, Alliance for an Energy Efficient Economy

– Sumedh Agarwal, Director, Smart and Resilient Power and Mobility, Alliance for an Energy Efficient Economy

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.