Our Terms & Conditions | Our Privacy Policy

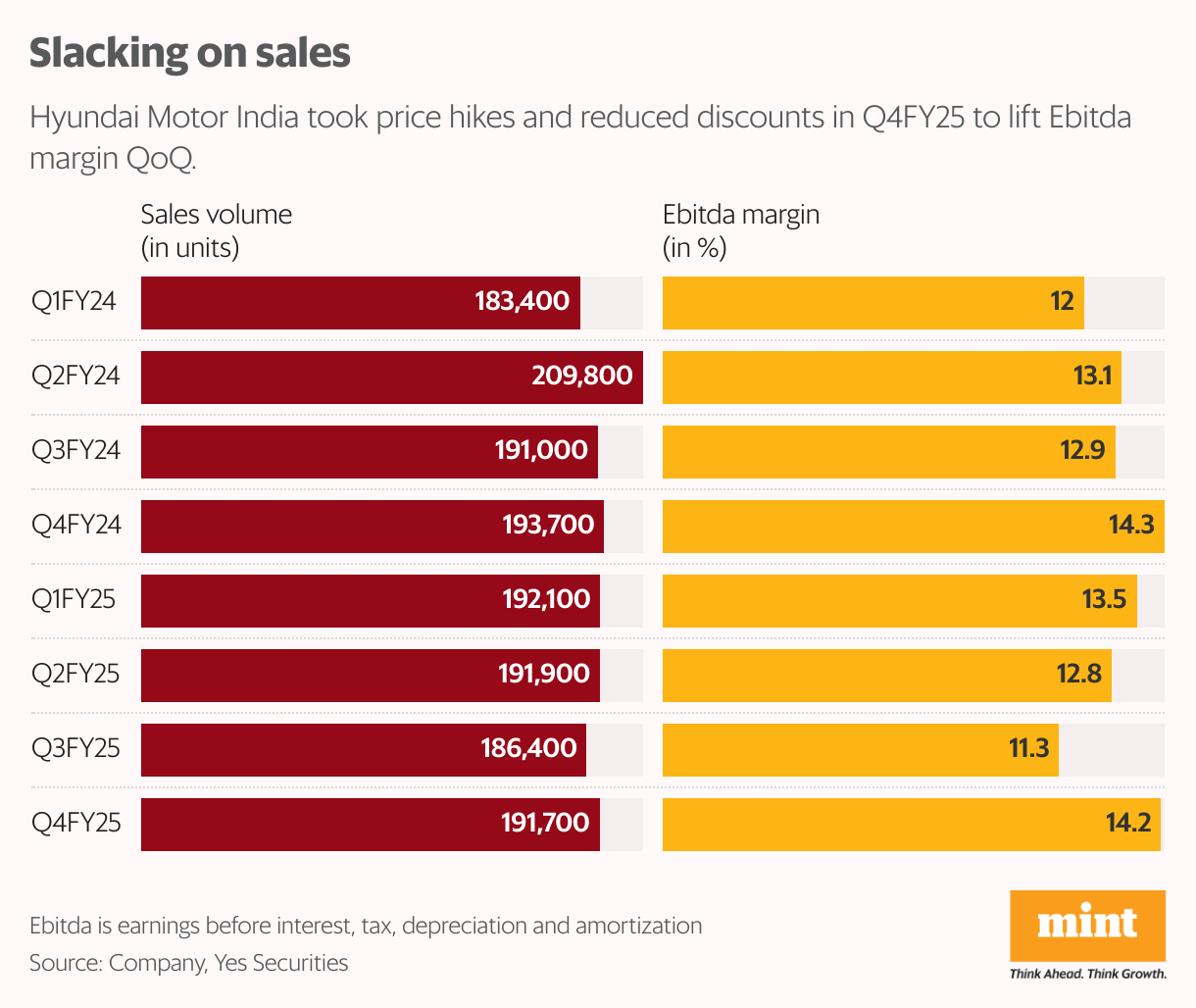

Hyundai Motor India Ltd has been hit hard by the waning popularity of hatchback cars in India. Its domestic sales volume fell by 4% year-on-year in the March quarter (Q4FY25) led by a steep 18% drop in hatchback volumes.

Export volumes saved the day, clocking 14% growth, keeping the company’s total volume largely stable at 191,650 units.

Average sales realization (blended for domestic and exports) increased 4.8% quarter-on-quarter to ₹8,94,792 per car. Year-on-year comparison showed the sales mix shifting in favour of a higher-priced SUV that benefits overall realization. So, it is better to look at the QoQ trend as the sales mix remained largely unchanged. Price hikes and lower discounts lifted realization. Consequently, Q4FY25 Ebitda margin rose QoQ by 271 basis points to 14.2% even though it was flattish year-on-year.

For FY26, the management expects low single-digit sales growth in the domestic market with export growth pegged at 7-8%. Hyundai aims to maintain a double-digit Ebitda margin in FY26. There could be some pressure on the net profit as depreciation from the commissioning of the Pune plant acquired from General Motors starts reflecting in accounts.

Focus on portfolio

Hyundai has chalked out separate strategies for expanding product portfolio in the short-term and long-term. Currently, it is not present in the hybrid car segment and plans to launch a model by September. Maruti Suzuki India Ltd and Toyota have hybrid car models of Grand Vitara and Hyrider respectively that use petrol engine and electric motor, and offer flexibility to use either mode. Hybrid vehicles help address the needs of buyers worried about the widespread availability of electric vehicle (EV) charging infrastructure with faster charging speed.

Hyundai hybrid car could be manufactured at the Pune plant, which is likely to start operations in H2FY26. The plant’s initial capacity is 170,000 vehicles, and is likely to be raised to 2,50,000 units by 2028.

Also read | ‘India to have 123 million EVs on the road by 2032 under best-case scenario’

Creta EV shines

Hyundai Creta EV, launched in Q4FY25, has been received well by consumers with most bookings for the long-range variant. According to the management, the EV is profitable for Hyundai if the launch-related marketing expenses and test drive discounts are ignored. It is focusing on localization strategy for battery cells in future to further boost the profitability of the model. Investors will closely track if Creta EV and the launch of hybrid car help Hyundai regain lost market share. Note that Hyundai’s market share based on wholesale volumes fell to 13.9% in FY25 from 14.6% a year ago.

In the long term, Hyundai has ambitious plans to expand its product portfolio by launching 26 new models by FY30, including 20 internal combustion engine vehicles and six EVs. The company is the export hub for emerging markets in Latin America and Africa. But the management is also open to exploring export opportunities in advanced countries such as Australia. Export sales volume is expected to increase to 30% of total sales in the long term from 21% at FY25-end, but this would also depend on how domestic sales evolve.

If Hyundai’s valuation is compared with larger peer Maruti, based on Bloomberg consensus estimates for FY26, it throws some interesting data. Both quote at a price-to-earnings multiple of about 25x, but Hyundai is cheaper on an EV/Ebitda basis at 15x versus 19x for Maruti.

What gives? Maruti’s other income is far higher, whereas its depreciation cost as a percentage of Ebitda is lower. Both these factors have a positive influence on its net profit. Hence, the right metric for valuing the core performance of both companies is EV/Ebitda.

Also read | EVs hit with falling resale value as consumer demand cools

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.