Our Terms & Conditions | Our Privacy Policy

(Editor’s note: John Hall is a professional commodities analyst.)

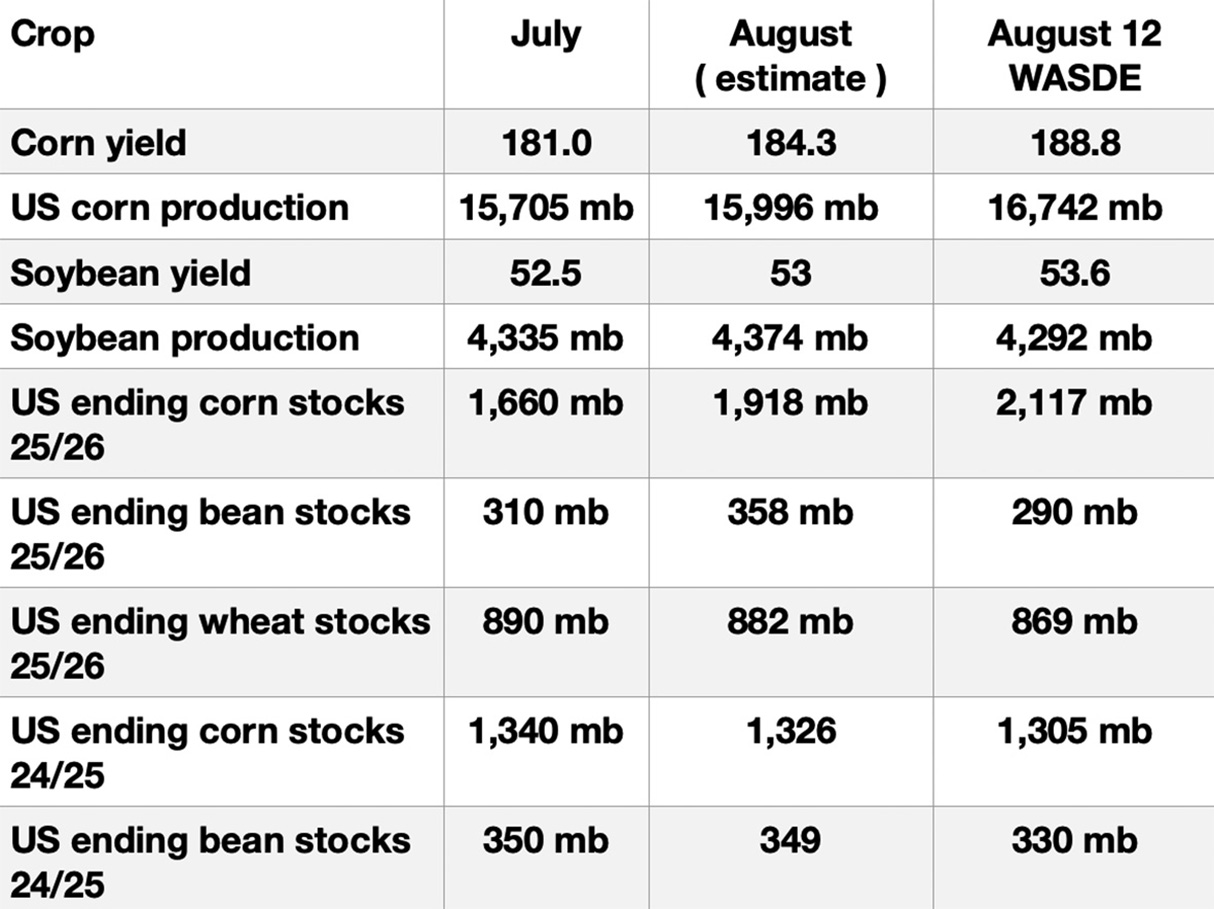

The World Agricultural Supply and Demand Estimate report released on Aug. 12 was a game changer.

I updated the summary table, seen at the right, that I shared last week and added the official numbers.

Note the projected corn yield and production. Note also what this increase in production did to new crop (2025-26) ending stocks.

A notable change came in planted acres for both corn (up) and beans (down).

The August report showed an increase of 2.051 million acres for corn 97,254 to 95,203.

The table seen on Page 10 from Karen Braun at Reuter, shows the states where the changes occurred.

Note that most of the increases came in the South. Remember the storms and wet weather they had in the south this spring?

It appears that growers in those areas felt they had sufficient moisture for corn this year.

As you would expect, the states that showed the increase in corn acres are basically the same states that lost bean acres.

Soybean acres in the report were reduced from 83.380 million down to 80.825 million (down 2.455 million acres).

To further throw water on a corn price rally I pulled the corn usage chart from the Department of Energy Alternative Fuels Data Center.

Take note that the U.S. corn usage chart, seen at the far right, has never topped 15 billion bushels and we are expected to produce over 16 billion this year. Enough said, the crop has a long way to go before it is in the bin.

On Aug. 14, December new crop corn closed at $3.93 — down eight cents since the report.

The nearby September contract closed at $3.70. New crop beans responded to the WASDE report and jumped 49 cents for the week and closed at $10.38.

The crop progress report released on Monday, Aug 11 had corn dropping a point to 72-percent Good to Excellent and beans also dropping a point to 68-percent Good to Excellent. The crop conditions posted support the increase in projected yields reported.

The popular Pro Farmer crop tour started on Aug. 18.

It will be interesting to see if their infield checks support the high yields currently projected.

Several reports last week have suggested China has been buying heavy from South America.

Because their crop (Brazil and Argentina) is harvested and in the bin, it is their time to make sales.

I am seeing several mixed reports coming from China so I don’t know how much buying they have actually done. It appears trade deals with Russia, India and China will have to be completed before we get a firm idea on market potential. U.S. Treasury Secretary Scott Bessent said on Aug. 12 that the Chinese talks will not reconvene for another two to three months.

In other news, you need to start watching the cost of phosphorus fertilizer as the talks with Russia/ Putin get underway. Russia supplies a good bit of the world’s phosphate.

EPA Secretary Lee Zeldin reported last week from the Iowa State Fair that changes will be coming in DEF / Diesel engines in the future.

(Note: I research material from Allendale, DTN, USDA, University Land Grants and other credible sources in compiling this article. It is not merely my opinion, but rather a consensus of experts in the trade. Looking for a marketing coach or someone to discuss strategies with? Contact me at jehgrain@gmail.com, or call 410-708-8781.)

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

Comments are closed.