Our Terms & Conditions | Our Privacy Policy

Why India’s creator economy is becoming every brand’s business | Advertising

India’s creator economy is not just a digital movement—it’s fast becoming a commercial powerhouse. As consumers increasingly turn to online voices for purchase cues, the lines between content and commerce are blurring, and brands are recalibrating their strategies accordingly. A new report by the Boston Consulting Group (BCG), From Content to Commerce: Mapping India’s Creator Economy, sheds light on the seismic shifts shaping this ecosystem. And the numbers are staggering.

According to BCG, India’s total consumption expenditure for FY2024 stands at $2,000 billion. Of this, creators are already influencing a chunk worth $350–$400 billion.

With consumer expenditure projected to double by FY2030, creator-influenced consumption is expected to triple—touching a monumental $1,000–$1,200 billion. In parallel, the direct revenues of the creator ecosystem are projected to grow fivefold—from $20–25 billion today to $100–125 billion by 2030.

Vipin Gupta, managing director and partner, BCG, puts it plainly, “India’s creator economy has the potential to significantly influence consumer spending, with creator-led spending set to account for 25–30% of India’s total consumer spend by 2030. What began as a Gen Z and metro-focused phenomenon is now resonating across age groups and smaller cities, unlocking new avenues of influence and engagement.”

Categories like fashion, beauty, and entertainment are leading the charge. At the same time, emerging monetisation models—such as live commerce and virtual gifting—are redefining how creators and brands drive value together.

A scale few can ignore

India’s creator economy is currently composed of 2 to 2.5 million active digital creators—defined as individuals with at least 1,000 followers—making it one of the world’s fastest-growing ecosystems. However, only 8–10% of them are currently monetising their content, underscoring a massive untapped opportunity.

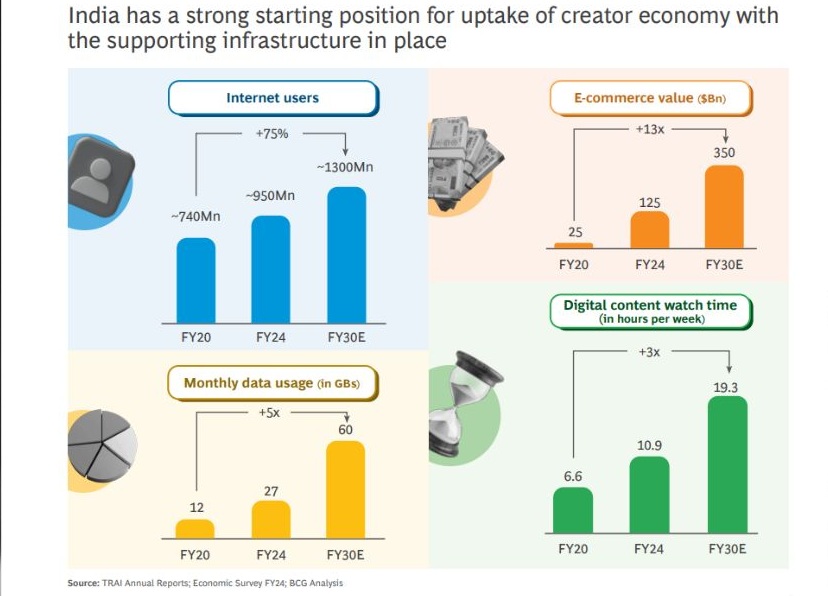

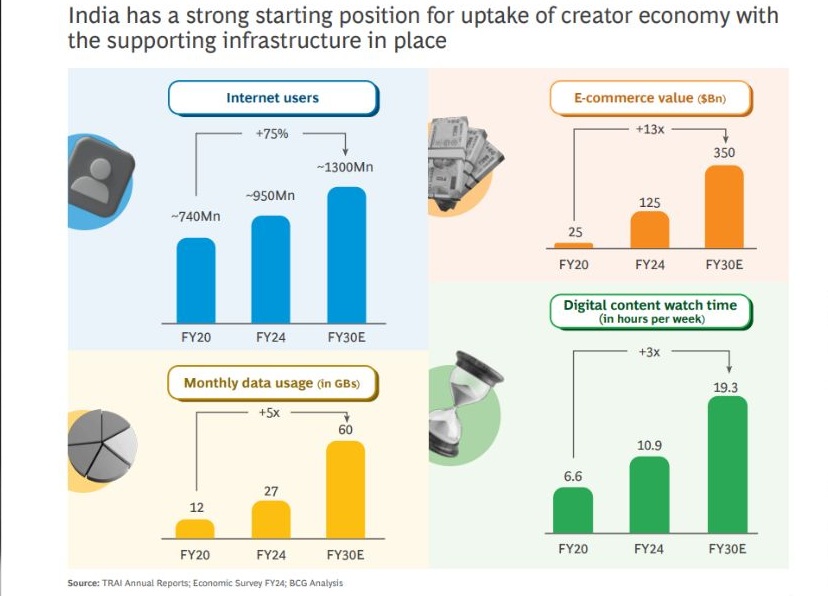

And it’s not just the metros. Consumption and content creation are booming in smaller cities.

“Our platforms of ShareChat and Moj have 75% of users and 80% of creators from Tier 2 and Tier 3 cities. We contribute to diversifying the creator and consumer profile for brands, while empowering regional creativity in India. We have also pioneered new monetisation models such as microtransactions, which drive the majority of creator earnings on our platforms today,” Manohar Singh Charan, co-founder, Moj and ShareChat noted in the study.

This shift has important implications for brands. As the ecosystem matures beyond metro-centric sensibilities, regional content and vernacular creativity are increasingly shaping consumer tastes. The potential to drive purchasing behaviour through influencer-led discovery is now more democratised—and also more complex.

The changing face of engagement

BCG’s research, which draws from a survey of over 1,900 consumers and 60 brands, found that 70% of online content consumption is driven by entertainment and information-seeking behaviours. Comedy, movies, daily soaps and fashion top the content genres. While lifestyle categories such as fashion, entertainment, and personal care dominate in terms of influence, sectors like home décor and financial services are still testing the waters.

Importantly, the creator economy’s appeal now spans across generations and city tiers. That means brands must revisit audience segmentation and rethink their engagement models.

“Creator marketing is increasingly becoming a cornerstone of brands’ marketing strategy, with budgets towards creator-led marketing expected to increase 1.5 to 3 times over the next 2–3 years. To fully leverage this potential, brands must trust creator-led outcomes, streamline decision-making, embrace agile content strategies, and invest in long-term creator partnerships,” Gupta added.

Follow the money: Monetisation moves beyond ads

Monetisation in the Indian creator space is no longer confined to branded partnerships. While beauty and fashion categories lead the pack, newer revenue streams such as virtual gifting, live commerce, and subscriptions are gaining traction—largely consumer-funded, and with scalable potential.

This diversification is likely to redefine how creators are valued—not merely by follower count, but by the richness of their engagement and their ability to drive transactions. However, brands must tread cautiously.

Monetisation may be diversifying, but it is still fragile. Only a fraction of creators are earning consistently, and many monetisation models, like live commerce, are still in experimental stages in India.

The brand imperative: Budget reallocation and new metrics

For marketers, the big takeaway is this: Creator-led marketing isn’t an experiment anymore—it’s a strategic pillar.

Currently, brands that engage in influencer marketing allocate 10–20% of their total marketing budgets to this channel. That share is set to increase rapidly, with 70% of surveyed brands planning to scale their creator budgets by 1.5 to 3 times over the next two to three years.

The objectives vary: 50% of brands use influencers for brand or product awareness, 70% aim to increase consumer consideration, 40% want to enhance brand loyalty and trust, and 28% are focused on boosting direct purchases through e-commerce or D2C channels.

Yet, hurdles remain. Chief among them are fake engagement (a concern for 74% of brands), lack of measurable ROI (40%), brand risk (38%), and mismatched content or audience targeting (20–22%). The ecosystem is still grappling with standardised performance metrics, making it challenging for marketers to build long-term strategies based on consistent, provable outcomes.

Why it’s not just about the creator anymore

To win in this environment, brands must move from tactical campaigns to strategic ecosystems. That involves building dedicated teams for creator collaboration, prioritising speed and agility in content production, and investing in robust vetting mechanisms to avoid the pitfalls of fake followers and misaligned content.

Globally, markets like Brazil and the U.S. show higher creator monetisation rates thanks to larger paying user bases and higher per capita content consumption. For India to reach that level of maturity, more investment is needed in digital literacy, creator training, and platform governance.

BCG’s report concludes that platforms, brands, and creators must “rethink strategies to stay ahead as the ecosystem matures. Faster content creation, greater creative freedom, diversified targeting, always-on outcome testing, and building specialised teams are essential to win with creators.”

India’s creator economy is at a crossroads. The opportunity is enormous, but the path forward will require a balancing act—between scale and quality, between reach and relevance, between short-term impact and long-term trust.

With over 30% of consumers already influenced by creators—and this figure set to rise dramatically—brands can no longer afford to treat this as an experimental channel. Done right, creator marketing can deliver authenticity, relatability, and measurable outcomes at a scale traditional media can’t match.

But this won’t be a plug-and-play solution. As creators grow in influence and revenue streams diversify, the creator economy will demand the same rigor, transparency, and accountability as any other media channel. For marketers, the call to action is clear: embrace creators not just as media vehicles, but as partners in building brand equity—across every screen, city, and consumer cohort.

[ad_1]

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

[ad_2]

Comments are closed.