Our Terms & Conditions | Our Privacy Policy

• Independent analysis: At current rate, country needs 11 years to achieve $1tr economy target

• Govt defends budget estimates, orthodox monetary policy • Increase transparency, cut cost of governance, govt urged

• Fiscal improvement more pronounced at state level, says report • 9.34m households receive N25,000 cash transfer

Nigeria’s ambitious N55 trillion budget and its path towards achieving a $1 trillion economy were laid before national economic managers, civil society groups, corporate leaders and international stakeholders yesterday, leaving many pondering the slim chances before the country, even as the grip on public revenue slips off.

As for the World Bank, which hosted the event to unveil its bi-annual Nigeria Development Update (NDU), the country has achieved a modest improvement – stabilising the foreign exchange reserves, raising business confidence and growing the public revenue-output ratio from 8.8 per cent share to 13.3 per cent last year, among other uptrends.

Still, it baulked at the prospect of achieving the $1 trillion economy target, noting that the feat could only be achieved if the country could quintuple its current growth rate.

The World Bank’s condition is a tall order for a country that is grappling with poor infrastructure required to accelerate business performance to grow tax revenue among other headwinds, such as poor public revenue.

But for post-COVID rebound, growth last year was at its fastest growth since 2014, when the current leading political party assumed leadership at the federal level. The economy closed the year at 3.4 per cent.

Earlier projections remained optimistic and suggested the speed could be sustained, but the bearish oil market and tariff crisis had added to the odds of sustaining the growth, with the International Monetary Fund (IMF) recently downgrading its projection to three per cent.

In nominal terms, the economy expanded by 17.1 per cent last year, growing from N229.9 trillion to N269.3 trillion (or $168.3 billion at the current exchange rate). If the country defies all odds and sustains last year’s growth, it will require 11 years to grow to achieve $995 billion (approximately $1 trillion).

This implies that the country would wait till 2036 as against the 2030 set government. But apart from pushing up the nominal growth rate, the government will also need to work at keeping the naira at its current exchange value (N1600/$).

If there is a significant depreciation of the currency, the country would need to wait longer to achieve the target or speed up growth far above 17 per cent nominal rate.

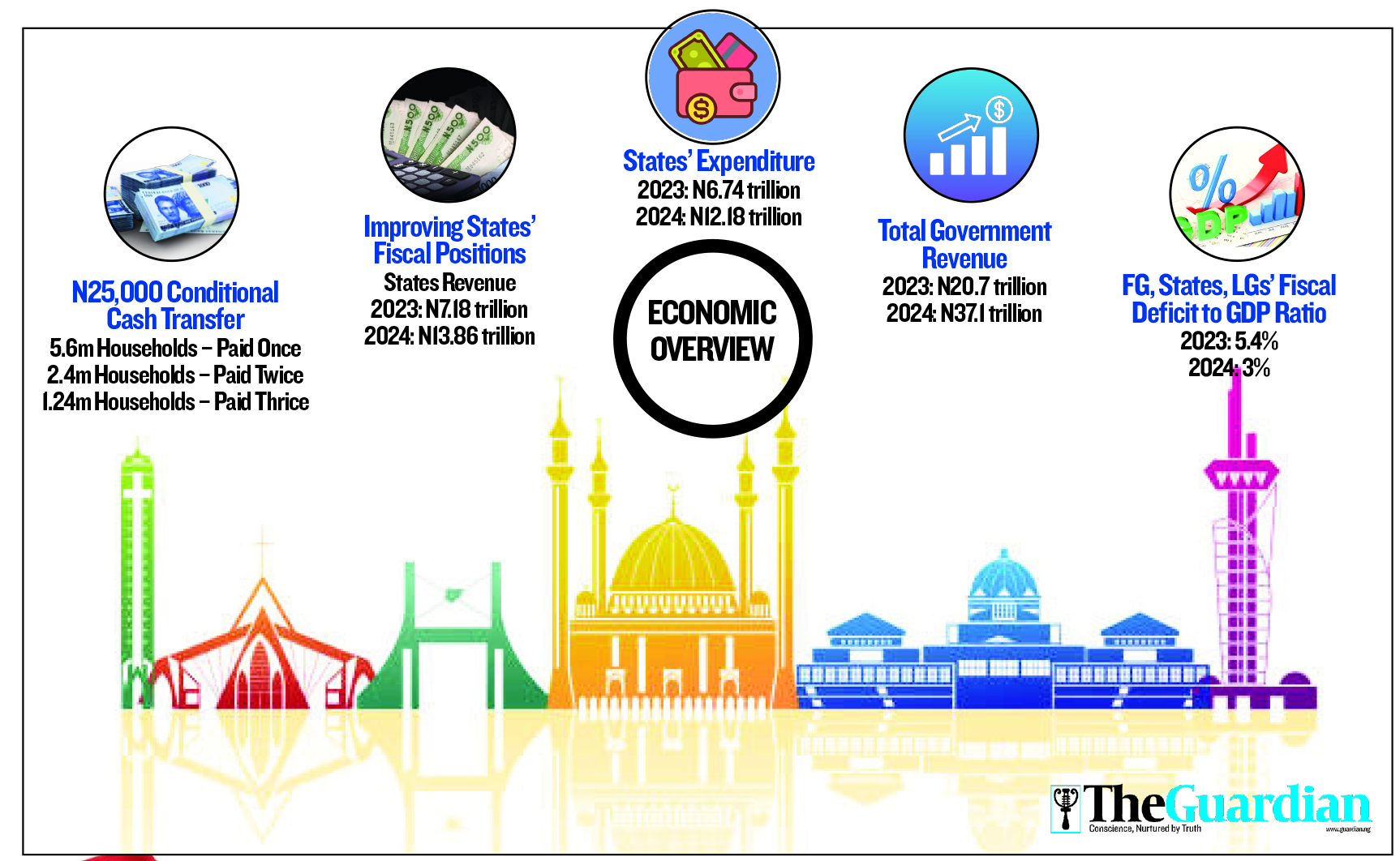

In the past three years, the naira has lost over 70 per cent of its value. This has pulled the country’s economy out of the African leadership position. The report also noted that the cash transfer programme has commenced but is slow. As of May 1, 5.6 million households were said to have received the N25,000 cash transfer once, while 2.4 million were paid twice, as against 1.24 million households that received the payment thrice. This suggests that 9.34 million households have received the conditional cash transfer.

To speed up development, it noted, economic reforms are necessary but not sufficient, while calling for sustained monetary tightening lower inflation, commitment to monetising fiscal deficits, improved balance sheet transparency, sustenance of market-reflective FX rates, increase transparency of oil revenue management and reduction in cost of governance.

Presenting the NDU report, themed ‘Building Momentum for Inclusive Growth’, the World Bank also expressed doubt about Nigeria’s ability to meet budgetary targets as contained in the 2025 budget estimates.

Beyond the self-set target, the report noted that the pace of growth would need to increase, expand prosperity and reduce poverty while rebalancing towards sectors and firms that are most productive, generate positive spillovers and create jobs and opportunities, especially for the poor and economically insecure.

For the Bretton Woods institution, though economic growth in the last quarter of 2024 increased to 4.6 per cent (year-on-year), pushing growth for the full year to 3.4 per cent, the highest since 2014 (excluding the 2021-2022 COVID-19 rebound), Nigeria does not have enough in its economic tanks to meets its development target.

The report also faulted the 2025 budget, which is described as overly ambitious in the face of crumbling oil prices.

“The FGN 2025 budget is overly ambitious, hence the need to carefully monitor its implementation and correct the course if needed. Overly optimistic revenue projections may cause financing requirements to exceed budgeted amounts, leading to a build-up of arrears and raising the risk of renewed recourse to deficit monetisation,” it stated.

It noted the upward trajectory of the government’s record in its economic reforms, saying that Nigeria’s macroeconomic situation is improving as a result of sustained reforms.

The reforms have helped to strengthen the foreign exchange market and Nigeria’s external position, it stated. The positive trend, it noted, resulted in the fiscal deficit shrinking from 5.4 per cent of GDP in 2023 to three per cent of GDP in 2024, driven by a sharp increase in revenues of the Federation, which rose from N16.8 trillion in 2023 (7.2 per cent of GDP) to an estimated N31.9 trillion in 2024 (11.5 per cent of GDP).

But it noted a dragnet of consolidating the macroeconomic stability and stimulating inclusive growth through deeper, wider structural reforms. The economy, as it is currently configured, is not generating jobs.

“There is a need for the economy to generate more and better jobs at scale and reduce poverty,” it noted. The report insisted that the best-performing sectors of the economy, like finance and ICT, are important drivers of growth, but are not sources of mass employment, as many Nigerians do not yet have the skills and opportunities to participate in them.

While it said a private sector-led and public sector-facilitated growth strategy could boost inclusive growth, the Bank urged Nigeria to address infrastructure gaps, such as in electricity and transportation, foster healthy competition, and market openness and improve the business environment to spur business dynamism.

According to the report, improving access to finance for new and existing firms to grow and improve productivity is key to unlocking Nigeria’s latent economic strengths.

It took note of the recently converging purchasing manager index of the Central Bank of Nigeria (CBN) and that of Stanbic IBTC, which are currently above 50 points, suggesting improved business confidence.

Until August last year, the CBN survey was above 50 points, while that of Stanbic IBTC, which is a private-sector-led study, was between 38 and 50 points.

The report also noted that external reserves have improved significantly following the “FX de facto unification”, which it put out in February last year (different from July 2023 when the FX liberalisation was executed). Its data also pointed to relatively closely converged official and parallel market rates.

It reports a significant improvement in the fiscal positions of the state government last year following the economic reforms, with their overall fiscal balance rising from N437 billion to N1.68 trillion, over 280 per cent increase.

The states, according to budget implementation reports (BIR) also increased total expenditure from N6.74 trillion to N12.2 trillion, while their revenue moved up from N7.2 trillion to N13.86 trillion. The reports, however, could not track or report the quality of sending items.

It noted that the reforms leave the states better off than the Federal Government in terms of fiscal improvement. In the face of improvement, it noted that prices remained high, with re-anchoring inflation expectations requiring “sustained monetary efforts” and fiscal coordination.

Delving into the report, the Acting World Bank Country Director for Nigeria, Taimur Samad, said: “Nigeria has made impressive strides to restore macroeconomic stability. With the improvement in the fiscal situation, Nigeria now has a historic opportunity to improve the quantity and quality of development spending, investing more in human capital, social protection, and infrastructure.

“The allocation of public resources can begin to shift away from the past unsustainable pattern, and rather towards meeting Nigeria’s large development needs, including the government playing its essential role of providing basic public services and serving as an enabler of the private sector–led growth.” World Bank Lead Economist for Nigeria, Alex Sienaert, submitted that improving policies in key sectors can help unleash the potential of these sectors.

“International experience suggests that the public sector cannot sustainably generate growth and jobs by itself. Nigeria is no exception, particularly since public resources remain constrained. A useful strategy is to position the public sector to play a dual role as a provider of essential public services, especially to build human capital and infrastructure and as an enabler for the private sector to invest, innovate and grow the economy,” he stated.

But providing rationalising the context of the 2025 budget estimates, the Minister of Budget and National Planning, Atiku Bagudu, insisted that the targets must not be met but present an opportunity for the government to push beyond its limits for maximum benefits of the country.

“A budget should not be a reflection of our indulgences. It should reflect our potential, as the President has noted. All of us are going to be challenged to give our best. The budget is supposed to get all organs of government to work harder and better. So that we can deliver prosperity,” he said.

The Minister of Finance and Coordinating Minister of the Economy, Wale Edun, stressed the importance of the government generating accurate data to drive the dissemination of correct information. Edun also mentioned that generating jobs and recording impacts on the lives of Nigerians will require investment.

“In terms of where we go next, the key is investment. It is an investment that allows productivity increases, that grows the economy, that creates jobs, high-quality jobs that lift Nigerians out of poverty in their millions, which is the aim of the President,” he explained.

On his part, the Governor of the Central Bank of Nigeria (CBN), Yemi Cardoso, took a jibe at Nigerians, saying: “I do feel that Nigerians perhaps do not read enough. They do not take advantage of useful analysis, which is readily available.” He stressed that the achievements recorded have vindicated his team’s insistence on adopting an ‘orthodox approach’ of the CBN.

Cardoso insisted that while the government must stay the course, achieving and sustaining market stability is important to maintain the momentum.

“I would say that clearly, for any economy, you do need stability for you to be able to grow. And we recognise our role as custodians of stability, and we recognise what we have to do to ensure that we accomplish and attain stability. Price stability and financial stability are very key areas that we must ensure that we are monitoring and that we get ahead of,” he said. He insisted that if the monetary policy continued the course of orthodox monetary policy, inflation would moderate soon.

The Minister of Communications and Digital Economy, Bosun Tijani, who defended the recent hike in telecoms tariffs, argued that Nigeria needs stable and efficient telecommunication technology to stabilise its financial services. He disclosed that telecommunication firms are investing about one billion in infrastructure, which was made possible by the hike in tariffs.

“There are currently orders for telecommunications equipment that are worth over $1 billion that have been placed. We are expecting some of the equipment to start coming into the country by June-July. This will improve the quality of connectivity in the country,” he added.

[ad_1]

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Aggregated From –

[ad_2]

Comments are closed.